Introduction: Why Roth IRA vs Traditional IRA Matters

Choosing between a Roth IRA vs Traditional IRA can feel confusing, especially when both accounts are designed for the same big goal: helping you build money for retirement. But the real difference is not just the name. The biggest difference is when you pay taxes.

A Traditional IRA may give you a tax break today. A Roth IRA may give you tax-free income later in retirement. That one difference can affect your paycheck, your tax refund, your retirement income, your Social Security taxes, and even how much flexibility you have later in life.

For 2026, the IRS says the total amount you can contribute to all your traditional and Roth IRAs combined is $7,500, or $8,600 if you are age 50 or older, subject to taxable compensation rules.

This guide explains Roth IRA vs Traditional IRA in simple, human language so you can understand which account may fit your situation better.

What Is an IRA?

An IRA, or Individual Retirement Arrangement, is a personal retirement savings account that gives tax advantages for setting aside money for retirement. The IRS describes an IRA as a personal savings plan with tax advantages.

Unlike a 401(k), which usually comes through an employer, an IRA is generally opened by you through a brokerage, bank, robo-advisor, or financial institution.

The two most common IRA types are:

- Traditional IRA

- Roth IRA

Both can help you invest in assets like mutual funds, ETFs, stocks, bonds, and index funds. But when comparing Roth IRA vs Traditional IRA, the real decision comes down to taxes, income limits, deduction rules, withdrawal rules, and future flexibility.

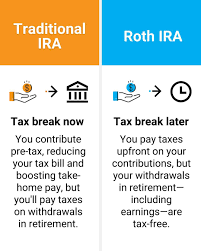

Roth IRA vs Traditional IRA: The Main Difference

The simplest way to understand Roth IRA vs Traditional IRA is this:

A Traditional IRA usually gives you tax benefits now, while a Roth IRA gives you tax benefits later.

With a Traditional IRA, your contribution may be tax-deductible. That means you may reduce your taxable income for the year you contribute. But when you withdraw money in retirement, deductible contributions and earnings are generally taxable.

With a Roth IRA, you contribute money after paying taxes. You usually do not get a tax deduction today. But qualified withdrawals in retirement can be tax-free.

So the question becomes:

Do you want the tax benefit today or in retirement?

That is the heart of the Roth IRA vs Traditional IRA decision.

Roth IRA vs Traditional IRA Quick Comparison Table

| Feature | Roth IRA | Traditional IRA |

|---|---|---|

| Tax benefit | Tax-free qualified withdrawals later | Possible tax deduction now |

| Contributions | Made with after-tax money | May be deductible |

| 2026 contribution limit | $7,500 / $8,600 age 50+ | $7,500 / $8,600 age 50+ |

| Income limits to contribute | Yes | No income limit to contribute, but deduction may be limited |

| Required minimum distributions | Not required for original owner | Generally required later in retirement |

| Best for | People expecting higher taxes later | People wanting tax savings now |

| Withdrawal flexibility | Contributions can generally be accessed more flexibly | Early withdrawals may trigger tax and penalty |

| Tax-free growth | Yes, if qualified | Tax-deferred growth |

2026 IRA Contribution Limits

For 2026, the combined annual contribution limit for all your Roth and Traditional IRAs is:

$7,500 if you are under age 50

$8,600 if you are age 50 or older

This is a combined limit. That means you cannot put $7,500 into a Roth IRA and another $7,500 into a Traditional IRA in the same year. Your total across both accounts must stay within the annual IRS limit.

For example, if you are 35 years old, you could contribute:

- $7,500 to a Roth IRA, or

- $7,500 to a Traditional IRA, or

- $4,000 to a Roth IRA and $3,500 to a Traditional IRA

But your total cannot exceed $7,500 for 2026 unless you qualify for the age 50+ catch-up amount.

This point is very important in the Roth IRA vs Traditional IRA debate because many beginners assume both accounts have separate limits. They do not.

Roth IRA Explained in Simple Words

A Roth IRA is a retirement account where you contribute money after paying taxes. You do not usually get a tax deduction when you contribute. The benefit comes later.

If you follow IRS rules, your qualified withdrawals can be tax-free in retirement. That means your investment growth may come out without federal income tax.

This can be powerful for younger investors, long-term investors, and people who believe their tax rate may be higher in the future.

Example:

Suppose you contribute $7,500 to a Roth IRA in 2026. You already paid tax on that income. If that money grows over many years, qualified withdrawals later may be tax-free.

That is why many people like the Roth IRA. It gives future tax freedom.

In the Roth IRA vs Traditional IRA comparison, the Roth IRA often wins when your current tax rate is low and your future tax rate may be higher.

Traditional IRA Explained in Simple Words

A Traditional IRA works differently. You may be able to deduct your contribution from taxable income now. This can lower your current tax bill.

But the money is not tax-free forever. Instead, it grows tax-deferred. You usually pay taxes when you withdraw the money in retirement.

Example:

Suppose you contribute $7,500 to a Traditional IRA in 2026 and qualify for a deduction. That contribution may reduce your taxable income for the year. If you are in a higher tax bracket today, that deduction could be valuable.

In the Roth IRA vs Traditional IRA decision, a Traditional IRA may be better if you need tax savings now and expect to be in a lower tax bracket during retirement.

Roth IRA Income Limits for 2026

A Roth IRA has income limits. If your income is too high, you may not be able to contribute directly.

For 2026, the Roth IRA income phase-out range is:

- Single or head of household: $153,000 to $168,000

- Married filing jointly: $242,000 to $252,000

- Married filing separately: $0 to $10,000

These are IRS phase-out ranges for Roth IRA eligibility.

This means if your income is below the lower number, you may be able to make a full contribution. If your income falls inside the range, your contribution may be reduced. If your income is above the upper number, you generally cannot contribute directly to a Roth IRA.

This is one reason high earners often compare Roth IRA vs Traditional IRA carefully. A Traditional IRA may still be available, but the deduction rules may be limited.

Traditional IRA Deduction Limits for 2026

A Traditional IRA does not have the same income limit for making contributions. But if you or your spouse is covered by a workplace retirement plan, your ability to deduct the contribution may be reduced.

For 2026, IRS traditional IRA deduction phase-out ranges include:

- Single taxpayers covered by a workplace retirement plan: $81,000 to $91,000

- Married filing jointly, contributor covered by a workplace plan: $129,000 to $149,000

- IRA contributor not covered by a workplace plan but married to someone who is covered: $242,000 to $252,000

- Married filing separately and covered by a workplace plan: $0 to $10,000

If neither you nor your spouse is covered by a retirement plan at work, the IRS says these deduction phase-outs do not apply.

This makes the Roth IRA vs Traditional IRA choice more personal. A Traditional IRA sounds attractive because of the tax deduction, but not everyone gets the full deduction.

Tax Benefits: Pay Now or Pay Later?

The biggest Roth IRA vs Traditional IRA question is simple:

Would you rather pay taxes now or later?

A Roth IRA asks you to pay taxes now. You contribute after-tax dollars. The reward is that qualified withdrawals may be tax-free later.

A Traditional IRA may reduce taxes now. You may get a deduction today, but withdrawals in retirement may be taxable.

Here is a simple way to think about it:

Choose a Roth IRA if you believe your tax rate may be higher in retirement.

Choose a Traditional IRA if you believe your tax rate is higher today and may be lower in retirement.

For example, a young worker early in their career may be in a lower tax bracket today. A Roth IRA may make sense because they pay tax now at a lower rate and potentially enjoy tax-free withdrawals decades later.

But a high-income worker near retirement may prefer a Traditional IRA deduction if they expect lower income after leaving work.

Withdrawal Rules: Roth IRA vs Traditional IRA

Withdrawals are another major difference in Roth IRA vs Traditional IRA planning.

With a Traditional IRA, deductible contributions and earnings are generally taxable when withdrawn. If you withdraw before age 59½, you may also face a 10% additional tax unless an exception applies.

With a Roth IRA, qualified withdrawals are generally tax-free. But if a withdrawal is not qualified, part of the distribution may be taxable, and early withdrawals may also face a 10% additional tax.

A Roth IRA is often seen as more flexible because contributions are made with after-tax money. However, earnings have stricter rules. To get the full tax-free benefit, you need to follow the qualified distribution rules.

This is where many beginners make mistakes. They hear “Roth IRA is tax-free” and assume every withdrawal is automatically tax-free. That is not always true. The withdrawal must meet IRS rules.

Required Minimum Distributions: A Big Retirement Difference

Required minimum distributions, or RMDs, are another key point in the Roth IRA vs Traditional IRA comparison.

Traditional IRAs generally require withdrawals later in retirement. These withdrawals can increase taxable income.

Roth IRAs are different. The IRS says Roth IRA owners are not required to take withdrawals while the account owner is alive, though beneficiaries may be subject to RMD rules.

This gives Roth IRAs a powerful advantage for people who want more control in retirement. If you do not need the money, you may leave it invested longer.

That flexibility can help with:

- Tax planning

- Estate planning

- Retirement income timing

- Avoiding unnecessary taxable income

- Leaving assets to heirs

In the Roth IRA vs Traditional IRA debate, this is one of the biggest long-term advantages of the Roth IRA.

Which Is Better for Young Investors?

For young investors, a Roth IRA often looks attractive.

Why? Because younger workers are often in lower tax brackets. They may not get a huge benefit from a tax deduction today. But they may benefit greatly from decades of tax-free growth.

Imagine a 25-year-old investor contributing every year to a Roth IRA. That money may have 30 to 40 years to grow. If withdrawals are qualified, the future tax savings could be meaningful.

A Roth IRA can also feel emotionally better for beginners because retirement withdrawals may be simpler. You already paid tax on the contribution. Later, qualified withdrawals may be tax-free.

For many young Americans comparing Roth IRA vs Traditional IRA, the Roth IRA may be the better long-term wealth-building tool.

Which Is Better for High-Income Earners?

For high-income earners, the answer is more complicated.

A Traditional IRA may offer a deduction, but the deduction may be reduced or eliminated if you are covered by a workplace plan and your income is above the IRS phase-out range.

A Roth IRA may also be limited because direct Roth contributions phase out at higher income levels.

So high-income earners need to look carefully at:

- Current tax bracket

- Workplace retirement plan coverage

- Roth IRA eligibility

- Traditional IRA deduction eligibility

- Future retirement tax rate

- Backdoor Roth strategy possibilities

- Existing pre-tax IRA balances

For high earners, Roth IRA vs Traditional IRA is less about which account sounds better and more about which one is actually available and tax-efficient.

Roth IRA vs Traditional IRA for Self-Employed Workers

Self-employed workers can also use IRAs, but they may have other retirement account options too, such as SEP IRAs, Solo 401(k)s, or SIMPLE IRAs.

Still, the Roth IRA vs Traditional IRA question matters. A self-employed person may have irregular income. In a lower-income year, Roth contributions may be attractive. In a higher-income year, a tax deduction may feel more valuable.

For example, if you are a freelancer, contractor, creator, consultant, or small business owner, your income may change every year. One year, you may prefer Roth. Another year, you may prefer Traditional.

That flexibility is useful. Retirement planning does not have to be one fixed decision forever.

Can You Have Both a Roth IRA and Traditional IRA?

Yes, you can have both a Roth IRA and a Traditional IRA. The IRS allows contributions to both, but your total annual contribution across both accounts cannot exceed the annual limit.

This can be a smart strategy for people who want tax diversification.

Tax diversification means having different types of retirement money:

- Taxable accounts

- Tax-deferred accounts

- Tax-free accounts

Having both Roth and Traditional money can give you more control later.

For example, in retirement, you may withdraw from a Traditional IRA in lower-tax years and use Roth IRA money in years when you want to avoid increasing taxable income.

That is why the Roth IRA vs Traditional IRA decision does not always have to be either-or. Sometimes, using both can be a smart middle path.

Common Mistakes to Avoid

Many people make avoidable mistakes when choosing between Roth IRA vs Traditional IRA.

One common mistake is contributing more than the allowed limit. The IRS says excess IRA contributions may be taxed at 6% per year for each year the excess amount remains in the IRA.

Another mistake is assuming Traditional IRA contributions are always deductible. They are not. Your deduction can depend on income, filing status, and workplace retirement plan coverage.

A third mistake is assuming Roth IRA withdrawals are always tax-free. Qualified withdrawals may be tax-free, but nonqualified withdrawals can create tax and penalty issues.

A fourth mistake is waiting too long. Retirement accounts work best when time is on your side. Even small contributions can grow meaningfully over decades.

A fifth mistake is choosing only based on today’s tax refund. A Traditional IRA deduction may feel good now, but the future tax cost also matters.

Roth IRA vs Traditional IRA: Which One Should You Choose?

Here is a simple decision guide.

A Roth IRA may be better if:

- You are young or early in your career

- Your current tax rate is low

- You expect higher taxes later

- You want tax-free qualified withdrawals

- You want more withdrawal flexibility

- You do not want lifetime RMDs as the original owner

- You are eligible under Roth IRA income limits

A Traditional IRA may be better if:

- You want a tax deduction today

- Your current tax rate is high

- You expect a lower tax rate in retirement

- You qualify for deductible contributions

- You need to reduce taxable income now

- You are closer to retirement and want current-year tax savings

When comparing Roth IRA vs Traditional IRA, the best account depends on your tax situation, income, age, retirement goals, and future expectations.

Example: Roth IRA vs Traditional IRA in Real Life

Let’s say Sarah is 28 years old, single, and earns $65,000 per year. She expects her income to rise over time. She is in a moderate tax bracket today and has decades before retirement.

For Sarah, a Roth IRA may be attractive because she can pay taxes now and potentially enjoy tax-free qualified withdrawals later.

Now let’s say Michael is 55 years old and earns $145,000 per year. He is in a higher tax bracket today and expects his income to drop after retirement. If he qualifies for a Traditional IRA deduction, he may prefer the current tax savings.

Both Sarah and Michael are making reasonable choices. They just have different situations.

That is the key lesson: Roth IRA vs Traditional IRA is not about which account is universally better. It is about which account is better for your life.

Best SEO-Friendly Summary for Beginners

If you are still confused, remember this:

A Roth IRA is usually better when you want tax-free retirement income later.

A Traditional IRA is usually better when you want a tax deduction now.

A Roth IRA is funded with after-tax money. A Traditional IRA may be funded with pre-tax or deductible money, depending on your eligibility.

A Roth IRA may give more flexibility in retirement because original owners do not have lifetime RMDs. A Traditional IRA can help reduce taxes today but may increase taxable income later.

The best choice is the one that matches your tax bracket, income level, and retirement goals.

Final Verdict: Roth IRA vs Traditional IRA

The Roth IRA vs Traditional IRA decision is one of the most important retirement choices Americans face. Both accounts can help you build wealth, but they work in different ways.

A Roth IRA may be better if you want future tax-free income, long-term flexibility, and no required withdrawals during your lifetime as the original owner. A Traditional IRA may be better if you want a tax break today and expect to be in a lower tax bracket later.

For 2026, the contribution limit is higher than previous years, giving savers more room to build retirement wealth. But income limits, deduction limits, withdrawal rules, and tax planning all matter.

Before choosing, ask yourself one simple question: Do I want my tax benefit now or later?

That answer will usually point you in the right direction.

Conclusion

Choosing between Roth IRA vs Traditional IRA is not about picking the account with the better name. It is about understanding your taxes, your income, your age, and your future retirement lifestyle. If you want tax savings today, a Traditional IRA may be useful. If you want tax-free qualified withdrawals later, a Roth IRA may be more powerful. For many people, the smartest retirement plan may even include both. The earlier you start, the more time your money has to grow, and that is where real retirement confidence begins.

Want to learn more about retirement planning and personal finance? Read more beginner-friendly guides on our personal finance blog.

“Hi, I am Devel Gupta, an entrepreneur and the founder of FinanceWithDevel. With 10 years of experience in teaching and simplifying personal finance, my mission is to help beginners build long-term wealth without the confusing jargon. Whether it’s budgeting, investing, or retirement planning, I believe financial freedom starts with simple, consistent habits. Let’s make money make sense. Connect with me on [ LinkedIn/Twitter ] for more daily tips!”