“With mortgage rates still above 6% and the median existing-home price above $400,000, many buyers need more than a down payment — they need financial breathing room.”

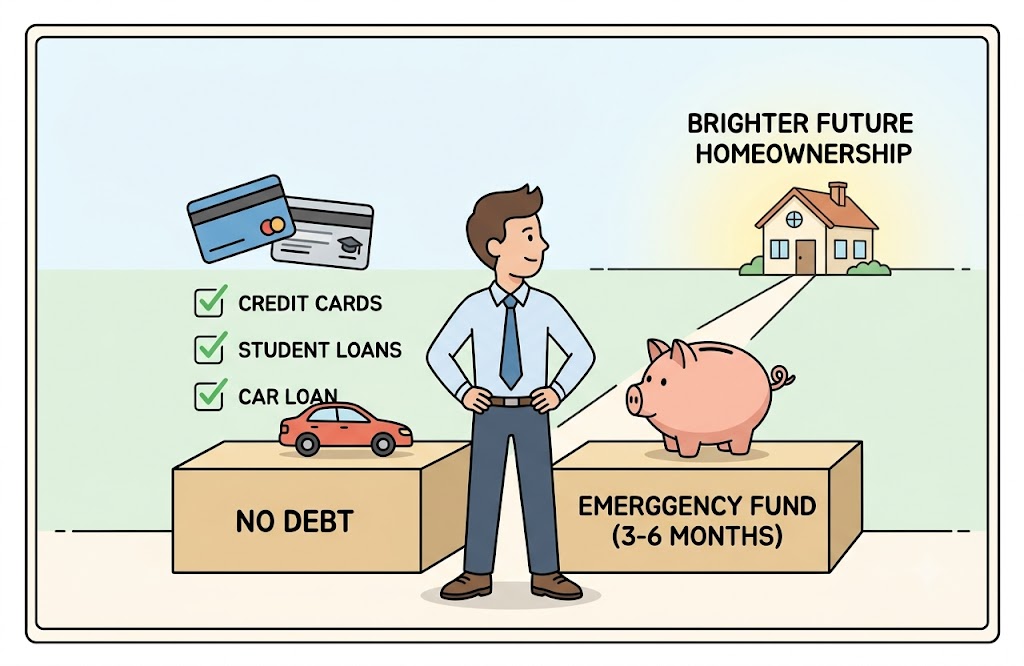

If Brandon wants to buy a house, the smartest thing he can do is not rush into saving for the down payment first. That sounds strange because most people think the first step to homeownership is stacking cash for the house. But the real first step is building a strong financial base. That is why no debt and emergency fund before buying a house is the main rule Brandon should follow. A house is not just a dream purchase; it is a long-term responsibility with monthly payments, repairs, taxes, insurance, and surprise bills that can hit at the worst possible time.

In the U.S., homeownership has become expensive enough that buyers need more than excitement. Freddie Mac reported the average 30-year fixed mortgage rate at 6.48% in early June 2026, which means borrowing is still costly compared with the low-rate years many people remember. NAR also reported a median existing-home price of $417,700 in April 2026, with prices still up year over year. When the house itself is expensive and the loan is expensive, Brandon cannot afford to be financially weak. This is exactly why no debt and emergency fund before buying a house is not boring advice; it is survival advice.

The Real Goal Is Not Just Buying a House

Brandon’s real goal should not be “How fast can I buy a house?” His real goal should be “How can I buy a house without destroying my peace?” There is a big difference. Anyone can get emotionally attached to a house listing, imagine the living room, dream about the backyard, and start calculating down payments. But a smart buyer thinks beyond the keys. A smart buyer asks, “Can I handle this house if life gets messy?” That is where no debt and emergency fund before buying a house becomes so important.

Debt makes Brandon’s life heavier before the mortgage even begins. If he already has credit card debt, a car loan, student loan payments, or personal loans, then his future mortgage is not his only obligation. His income is already divided into many pieces. Add a mortgage on top, and suddenly every paycheck feels like it disappears. A house should feel like progress, not pressure. That is why Brandon needs to clear debt first and keep a separate cash cushion for emergencies.

Think of Brandon’s finances like a bridge. The house is the heavy truck crossing that bridge. If the bridge is weak, the truck may technically get on it, but the structure is under stress. Debt weakens the bridge. No savings weakens it even more. But no debt and emergency fund before buying a house strengthens the bridge before the heavy truck arrives.

Why Debt Is a Problem Before Homeownership

Debt is not just a number on a statement. Debt is a monthly claim on Brandon’s future income. Every payment he owes is money he cannot use for mortgage payments, utilities, repairs, savings, investing, or life. If Brandon has a $450 car payment, a $200 credit card minimum, and a $300 personal loan payment, that is $950 per month already gone. Now add a mortgage, property taxes, homeowners insurance, HOA fees, utilities, and maintenance. That monthly budget can get tight fast.

Example:

Brandon has $6,000 in credit card debt at 24% APR. Even if he qualifies for a mortgage, that debt can drain hundreds of dollars per month and make repairs harder to handle after closing.

Mortgage lenders also care about debt because it affects Brandon’s debt-to-income ratio. The Consumer Financial Protection Bureau explains that debt-to-income ratio compares monthly debt payments with gross monthly income, and lenders use it to evaluate whether someone can manage monthly payments. Even if Brandon feels confident emotionally, the numbers may tell another story. This is why no debt and emergency fund before buying a house helps him look stronger to lenders and feel stronger in real life.

Debt also creates stress. When someone owes money, they are not fully free to make choices. They are always working around payments. They may want to save, but the credit card bill shows up. They may want to invest, but the car loan takes priority. They may want to repair the home, but old debt blocks the budget. Brandon should not bring that stress into homeownership if he can avoid it.

Why an Emergency Fund Must Come Before House Savings

An emergency fund is Brandon’s financial shock absorber. Without it, every unexpected problem can turn into new debt. A medical bill, job loss, car repair, broken appliance, plumbing issue, or roof leak can quickly become a credit card balance. For renters, some repairs are the landlord’s problem. For homeowners, those repairs become Brandon’s problem. That is a huge shift. This is why no debt and emergency fund before buying a house is one of the best homebuying rules for beginners.

Bankrate says an emergency fund helps cover unplanned expenses such as job loss, medical bills, or car repairs, and notes that three to six months of essential expenses is often recommended. Bankrate also reports that only 46% of U.S. adults have enough emergency savings to cover three months of expenses, while 24% have no emergency savings at all. That means many Americans are financially exposed. Brandon should not join that group right before buying one of the biggest assets of his life.

A 3–6 month emergency fund gives Brandon breathing room. If he loses income, he has time. If the HVAC system breaks, he has options. If his car needs repairs, he does not have to choose between transportation and the mortgage. No debt and emergency fund before buying a house gives Brandon a cushion between normal life and financial chaos.

What 3–6 Months of Emergency Savings Really Means

A 3–6 month emergency fund does not mean Brandon needs to save 3–6 months of luxury spending. It means he should save 3–6 months of essential expenses. That includes housing, groceries, utilities, insurance, transportation, minimum medical needs, and basic communication bills. It does not include vacations, eating out, shopping, entertainment, or lifestyle upgrades. The emergency fund is not designed to preserve every comfort. It is designed to keep Brandon safe during a crisis.

For example, if Brandon’s essential monthly expenses are $3,500, then a three-month fund would be $10,500, and a six-month fund would be $21,000. If Brandon has a stable job, no dependents, and low monthly expenses, three months may be a good starting point. If his income is unstable, he supports family, works in a risky industry, or simply sleeps better with more safety, six months is smarter. The phrase no debt and emergency fund before buying a house means Brandon should build the version of safety that fits his actual life.

This money should stay separate from the down payment. That part is extremely important. If Brandon saves $30,000 and uses all of it for the house, he may technically close on the property but start homeownership with no shield. That is not smart. A down payment helps Brandon buy the house. An emergency fund helps Brandon keep the house.

The Housing Market Makes This Rule Even More Important

The current U.S. housing market is not exactly handing out easy wins to first-time buyers. Rates are still elevated, home prices are still high, and buyers must think carefully about affordability. NAR reported 1.47 million unsold units in April 2026, equal to 4.4 months of supply, but the median existing-home price was still $417,700. More inventory may give buyers more choices, but it does not magically make homeownership cheap. Brandon still needs cash, discipline, and a plan.

This is why no debt and emergency fund before buying a house matters even more today. When mortgage rates are high, a small difference in loan amount or interest rate can change the monthly payment in a big way. When prices are high, closing costs and down payments also become heavier. If Brandon buys without preparation, he may become “house poor,” which means he owns a home but has little cash left for anything else. That is not financial freedom. That is financial pressure wearing a nice front-door keychain.

A strong buyer is not just the person with the biggest loan approval. A strong buyer is the person who can still pay bills, handle repairs, and save after closing. Brandon should aim to be that buyer. The market may be tough, but no debt and emergency fund before buying a house gives him a better shot at staying calm and stable.

Debt-Free Brandon vs Debt-Heavy Brandon

| Situation | Brandon With No Debt + Emergency Fund | Brandon With Debt + No Emergency Fund |

|---|---|---|

| Monthly budget | More breathing room | Tight and stressful |

| Mortgage approval | Cleaner financial profile | Higher debt-to-income pressure |

| Repair costs | Can use savings | May use credit cards |

| Job loss | Has a cash buffer | May miss payments quickly |

| Emotional stress | More confidence | More anxiety |

| Long-term wealth | Easier to save and invest | Debt keeps pulling money backward |

This table shows the real difference. Brandon with no debt and emergency fund before buying a house is not just “better with money.” He is safer. He can make decisions slowly, compare homes carefully, and avoid desperation. Brandon with debt and no savings may feel excited at first, but the first major bill can shake everything.

How Debt Can Make the House More Expensive

Debt can make the house more expensive indirectly because it limits Brandon’s choices. If his debt-to-income ratio is high, he may not qualify for the loan amount he wants. If he does qualify, the monthly payment may still feel uncomfortable because his old debt remains. Even worse, if he carries credit card debt after buying, home repairs may push him deeper into interest payments. That is how a house can become more expensive than the price tag suggests.

There is also opportunity cost. Money going toward debt cannot go toward the down payment. Money going toward interest cannot go toward investments. Money going toward old purchases cannot go toward future stability. This is why no debt and emergency fund before buying a house is such a powerful concept. It removes financial drag before Brandon takes on a mortgage.

Imagine Brandon trying to run uphill while dragging a suitcase full of rocks. That suitcase is debt. He might still move forward, but everything takes more effort. Paying off debt first is like dropping the suitcase. Suddenly, saving for the house becomes faster, lighter, and more realistic.

Why Emergency Savings Protect the Mortgage

A mortgage is usually the biggest monthly payment in a household budget. Missing it can damage credit, create late fees, and eventually put the home at risk. Emergency savings protect Brandon from that outcome. If his income drops or expenses spike, the emergency fund gives him time to adjust without immediately falling behind. That is why no debt and emergency fund before buying a house is not just about buying the home; it is about protecting the home.

The Federal Reserve’s 2026 report said 73% of adults were either doing okay or living comfortably, but only 63% could cover a $400 emergency expense using cash or its equivalent. It also said prices remained the most common financial concern among U.S. adults. This shows how fragile many budgets can be even when people appear to be doing okay. Brandon should not assume a good income alone is enough. Income helps, but savings protects.

A home has a way of creating emergencies. The dishwasher does not ask whether Brandon’s budget is ready. The roof does not wait until bonus season. The car does not break down after checking his savings balance. No debt and emergency fund before buying a house helps Brandon handle these moments without panic.

The Right Order for Brandon’s Money

Brandon should follow a simple order: clear high-interest debt, build the emergency fund, then save for the house. This order may not feel exciting, but it works. Personal finance is not about looking rich for five minutes. It is about becoming stable for years. The right order keeps Brandon from building a dream on top of stress.

First, Brandon should pay off credit cards and high-interest loans. Second, he should build a 3–6 month emergency fund in a safe, liquid account. Third, he should save for the down payment. Fourth, he should save for closing costs, moving expenses, and basic repairs. The rule no debt and emergency fund before buying a house fits perfectly into this order because it keeps the foundation stronger than the dream.

Once debt is gone, Brandon can redirect those old payments into savings. If he was paying $700 per month toward debt, that $700 can now build his emergency fund. After the emergency fund is complete, the same $700 can go toward the down payment. This is how slow discipline becomes fast progress.

Step 1: Pay Off High-Interest Debt

Brandon should begin with high-interest debt because it usually works against him the hardest. Credit cards, personal loans, and expensive financing plans can eat his income quietly. The interest does not feel dramatic on day one, but over months and years, it becomes a money leak. If Brandon wants no debt and emergency fund before buying a house, this is where the cleanup starts.

He can use the avalanche method by paying the highest-interest debt first, or the snowball method by paying the smallest balance first. The avalanche method saves more interest mathematically. The snowball method can feel more motivating because quick wins build confidence. Brandon does not need a perfect method. He needs a method he will actually follow until the debt is gone.

During this phase, Brandon should avoid taking on new payments. No unnecessary car upgrades. No furniture financing. No “buy now, pay later” shopping. A future homeowner needs strong habits before strong walls. If Brandon cannot say no to small debt now, a big mortgage later will not magically fix that behavior.

Step 2: Build the Emergency Fund

After high-interest debt is gone, Brandon should build his emergency fund with focus. This money should sit in a safe place, such as a savings account or high-yield savings account. It should not be invested in stocks, crypto, or anything that can drop in value right when he needs it. Emergency money has one job: be available. That is why no debt and emergency fund before buying a house is about safety, not chasing high returns.

Brandon should calculate his essential monthly expenses and multiply that number by three, then by six. That gives him a target range. If his monthly essentials are $3,000, he needs $9,000 to $18,000. If his monthly essentials are $4,500, he needs $13,500 to $27,000. These numbers may look big, but they are smaller than the cost of a financial disaster.

He should automate savings if possible. Even $100, $250, or $500 per month creates momentum. Bonuses, tax refunds, side income, or unused budget money can speed up the process. The key is to protect the fund once it exists. Brandon should not treat emergency savings like a vacation account. No debt and emergency fund before buying a house only works if the emergency fund remains untouched for real emergencies.

Step 3: Save for the House the Smart Way

Once Brandon is debt-free and has emergency savings, then house saving becomes powerful. Now he can save without fear. He is not choosing between credit card bills and the down payment. He is not one emergency away from draining everything. He is finally saving from a position of strength. This is the moment when no debt and emergency fund before buying a house turns from advice into real confidence.

Brandon should save for the down payment, closing costs, inspection, appraisal, moving expenses, utility setup, furniture basics, and early repairs. Many buyers forget the “after closing” costs. They spend everything to get into the house and then use credit cards to live in it. Brandon should avoid that trap. The move-in fund is not optional; it is part of buying wisely.

He should also decide his comfortable monthly payment before getting emotionally attached to homes. The lender may approve one number, but Brandon’s life may require a lower number. He should leave room for investing, retirement savings, repairs, insurance increases, property tax changes, and normal fun. A house should not turn Brandon into a prisoner of his own budget.

How Much House Should Brandon Really Buy?

Brandon should buy less than the maximum he can qualify for. This is one of the quiet secrets of peaceful homeownership. The bank looks at risk from the lender’s side. Brandon must look at life from his side. He knows his goals, family responsibilities, job stability, lifestyle, and stress level better than any approval formula. That is why no debt and emergency fund before buying a house should be paired with conservative affordability.

Example:

If Brandon takes home $5,500 per month, he may not want a $3,000 housing payment even if a lender approves him. After groceries, insurance, utilities, car costs, repairs, and savings, that payment could make him house poor.

A good homebuying budget should include principal, interest, taxes, insurance, HOA fees if any, utilities, maintenance, and savings after closing. If the payment leaves no room for repairs or investing, the house is probably too expensive. If Brandon has to stop retirement contributions just to afford the mortgage, he should slow down. Homeownership is valuable, but it should not cancel every other financial goal.

The best house is not always the biggest house. The best house is the one Brandon can afford during good months and bad months. A slightly smaller home with a calm budget is better than a dream home that creates constant stress. No debt and emergency fund before buying a house helps Brandon choose wisely instead of emotionally.

Common Mistakes Brandon Should Avoid

The biggest mistake Brandon can make is using his emergency fund as part of the down payment. That may help him buy sooner, but it leaves him exposed immediately after closing. Another mistake is ignoring small debts because they seem harmless. Small debts become big pressure when a mortgage enters the budget. A third mistake is trusting lender approval more than personal affordability.

Brandon should also avoid comparing himself to friends, coworkers, or influencers. Someone else may buy sooner because they have family help, higher income, lower expenses, or hidden debt. Social media does not show the full budget. It shows the kitchen island, the keys, and the smiling photo. Brandon needs to care more about his real numbers than someone else’s highlight reel. That is why no debt and emergency fund before buying a house keeps him grounded.

He should also avoid rushing because he fears prices will rise forever. Fear-based buying is dangerous. Yes, prices can rise. Yes, rates can change. But buying before he is ready can cost more than waiting. A rushed purchase with debt and no savings can create years of stress. A patient purchase with a strong foundation can create long-term wealth.

Financial Disclaimer

This article is for educational and informational purposes only and should not be considered personal financial, mortgage, tax, legal, or investment advice. Homebuying decisions depend on many personal factors, including income, debt, credit score, savings, mortgage rate, location, loan type, family needs, and long-term financial goals.

Before buying a house, paying off debt, choosing a mortgage, or using savings for a down payment, consider speaking with a qualified financial advisor, mortgage professional, tax expert, or HUD-approved housing counselor. Every buyer’s situation is different, and what works for one person may not be the best choice for another.

This article does not guarantee loan approval, lower costs, or financial success. Always review your own budget carefully and make decisions based on your personal financial situation.

Final Thoughts

Brandon should have no debt and emergency fund before buying a house because a home is not just a milestone; it is a responsibility. Debt makes the budget tight. No savings makes surprises dangerous. But debt freedom and emergency savings give Brandon control. They help him qualify more comfortably, handle repairs, survive income shocks, and enjoy the home instead of fearing every bill.

The U.S. housing market is still expensive, and the numbers prove it. Mortgage rates remain meaningful, home prices remain high, and many Americans are still underprepared for emergencies. Brandon does not need to follow the crowd into financial stress. He can follow a smarter order: pay off debt, build emergency savings, then save for the house.

A home should feel like a blessing, not a burden. If Brandon follows the rule of no debt and emergency fund before buying a house, he gives himself the best chance to become not just a homeowner, but a stable homeowner. And that is the real win.

FAQs

1. Why should Brandon have no debt before buying a house?

Brandon should have no debt before buying a house because debt reduces monthly cash flow and can weaken his mortgage application. Existing debt payments also make it harder to handle repairs, utilities, insurance, and other homeownership costs. The rule no debt and emergency fund before buying a house helps Brandon start homeownership with less stress and more control.

2. How much emergency fund should Brandon save before buying?

Brandon should save 3–6 months of essential expenses before buying. Essential expenses include housing, food, utilities, insurance, transportation, and basic needs. If his expenses are $3,500 per month, then a good emergency fund target is $10,500 to $21,000. This is why no debt and emergency fund before buying a house is such a practical rule.

3. Can Brandon save for a house while paying off debt?

Brandon can save a small starter amount, but high-interest debt should usually come first. If he saves for a down payment while credit card interest grows, he may not be making real progress. Paying off debt first makes future house saving faster and cleaner. That is the logic behind no debt and emergency fund before buying a house.

4. Should Brandon use his emergency fund for the down payment?

No, Brandon should not use his emergency fund for the down payment. The emergency fund should stay separate because it protects him after closing. If he spends all his cash buying the house, one repair or income problem can push him into debt. No debt and emergency fund before buying a house means both the house fund and emergency fund have separate jobs.

5. What should Brandon do after becoming debt-free and saving an emergency fund?

After Brandon becomes debt-free and saves 3–6 months of expenses, he can start saving for the down payment, closing costs, moving costs, and early home repairs. He should also choose a mortgage payment that fits his real budget, not just the lender’s approval amount. Once he follows no debt and emergency fund before buying a house, he can shop with confidence instead of pressure.

Can Brandon buy a house if he still has student loans?

Yes, but he should check his DTI, emergency fund, monthly cash flow, and loan stability first. Student loans are not always a deal-breaker, but high-interest debt and no savings can make homeownership riskier.

“Hi, I am Devel Gupta, an entrepreneur and the founder of FinanceWithDevel. With 10 years of experience in teaching and simplifying personal finance, my mission is to help beginners build long-term wealth without the confusing jargon. Whether it’s budgeting, investing, or retirement planning, I believe financial freedom starts with simple, consistent habits. Let’s make money make sense. Connect with me on [ LinkedIn/Twitter ] for more daily tips!”