Money advice is everywhere in 2026. Open TikTok, YouTube, Reddit, Google, newsletters, podcasts, or AI tools, and someone is ready to tell you how to invest, save, retire early, lower taxes, buy insurance, beat inflation, or build wealth. Some advice is helpful, but some of it is rushed, sponsored, incomplete, or built mainly for clicks. That is why Kiplinger’s Personal Finance still matters for U.S. readers who want practical guidance instead of financial noise. It gives readers a slower, more organised way to think about decisions that can affect retirement, taxes, investments, insurance, and family budgets.

This does not mean one publication should run your financial life. No article, magazine, influencer, app, or AI answer can know your full income, debt, tax situation, age, family needs, risk tolerance, or goals. But when Americans are dealing with higher living costs, changing retirement rules, Social Security concerns, confusing insurance premiums, and constant online money opinions, a careful source becomes useful. This kind of guide works best as a trusted starting point: a place to understand the issue, learn the vocabulary, compare choices, and then decide what fits your own situation.

What is Kiplinger’s Personal Finance

Kiplinger’s Personal Finance is a U.S. money publication that covers investing, taxes, retirement, saving, insurance, real estate, college costs, Social Security, estate planning, and major household decisions. According to Kiplinger’s official About page, the Kiplinger brand dates back to 1920 and focuses on practical financial guidance for individuals, investors, and professionals. Ohio University’s Kiplinger history page also notes that Kiplinger Magazine, now known as the personal finance magazine, began in 1947. That long publishing history matters because personal finance is not a trend; it is a lifelong skill.

For readers, the value is not just history. The real value is structure. Personal finance often feels like a messy kitchen drawer, cluttered with random pieces like:

- Tax Forms & Limits (Keeping up with annual IRS changes)

- Retirement Accounts (Navigating 401(k) choices and Roth IRA rules)

- Government Benefits (Deciding the right Social Security timing)

- Safety Nets (Building emergency funds and reviewing insurance renewals)

- Long-Term Planning (Handling mortgage decisions and estate documents)

- A good guide helps you pull those pieces out one by one and understand how they connect. The publication is useful because it treats money as a system rather than a pile of random hacks.

Why have readers trusted Kiplinger’s Personal Finance for years

Trust in financial content does not come from loud headlines. It comes from accuracy, consistency, editorial standards, source checking, and the habit of explaining trade-offs. Kiplinger’s Personal Finance has built much of its reputation by focusing on usable guidance: how to save more, how to think about taxes, how to plan retirement income, how to compare financial products, and how to avoid common money mistakes. That type of content may not feel as exciting as a viral “get rich fast” video, but it is often much more useful.

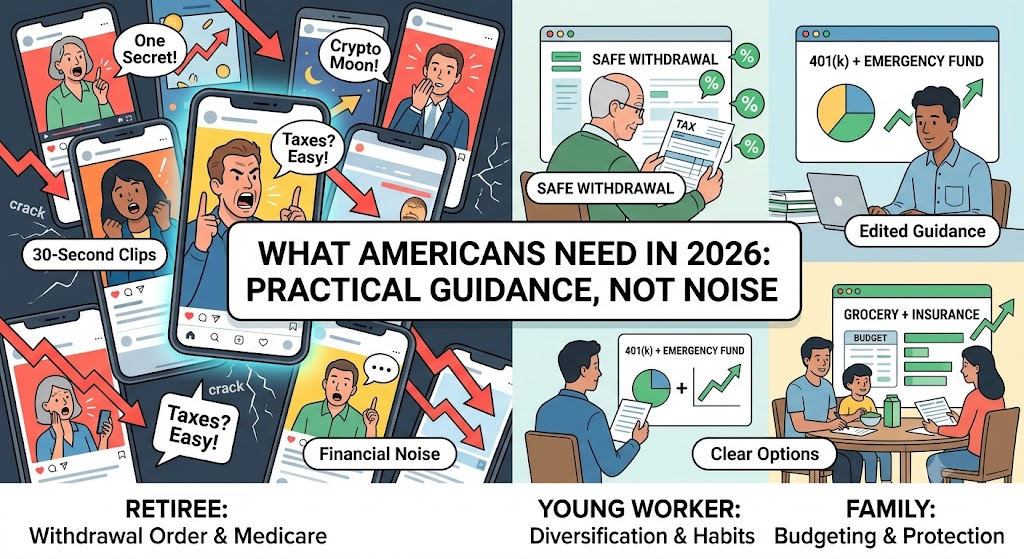

This matters because real financial decisions are rarely simple. A retiree does not need a 30-second clip promising one secret to avoid all taxes. A young worker does not need someone shouting that one stock, coin, or side hustle will solve everything. A family dealing with grocery bills, rent, insurance, gas, and school costs needs clear options. This type of money guidance is valuable when it explains the boring but important details that can quietly shape a household’s future.

Why It Still Matters in 2026

The internet has made financial information easier to access, but it has also made bad information easier to spread. A 2025 TIAA Institute-GFLEC report found that U.S. adults correctly answered only 49% of financial literacy questions on average, showing that many people still struggle with risk, borrowing, saving, investing, and retirement concepts. At the same time, Pew Research Centre data shows many Americans regularly get news from social media platforms such as Facebook, YouTube, Instagram, and TikTok. That creates a big problem: people are getting more money content, but not always better money judgment.

This is where Kiplinger’s Personal Finance still has a role. It gives readers a more edited, context-heavy place to start before they make decisions involving taxes, retirement income, debt, Social Security, or investment risk. Social media is like a crowded food court: some stalls serve healthy meals, some sell dessert, and some are just reheating yesterday’s leftovers with bright signs. A serious personal finance source helps readers ask better questions before buying into the loudest pitch.

What Topics Does Kiplinger’s Personal Finance cover

A strong personal finance publication should follow the money questions people actually ask at different life stages. Kiplinger’s Personal Finance commonly covers core financial pillars, including:

- Retirement Planning: Social Security timing, Medicare, and pension strategies.

- Investing & Wealth Building: Understanding 401(k)s, IRAs, and diversification.

- Tax Optimisation: Tax-smart withdrawal strategies and updates on IRS limits.

- Daily Money Management: Household budgeting, insurance comparison, and tackling inflation.

The 2026 environment makes these topics even more important. The IRS announced that the 401(k) employee contribution limit increased to $24,500 for 2026, while the IRA contribution limit increased to $7,500. The Social Security Trustees have projected pressure on the OASI trust fund, making Social Security planning a serious topic for future retirees. The Bureau of Labour Statistics reported that the Consumer Price Index for All Urban Consumers rose 3.8% over the 12 months ending April 2026, showing why inflation still matters for household budgets. Kiplinger’s Personal Finance helps readers connect those official numbers to everyday choices.

Traditional Money Guidance vs Online Finance Influencers

Online creators can be excellent teachers. Some explain credit scores, index funds, budgeting, debt payoff, and retirement accounts in a friendly way that traditional media sometimes failed to do. The problem is that influencer content may also be shaped by sponsorships, affiliate links, personal bias, limited disclosures, or advice that fits the creator’s life but not yours. Kiplinger’s Personal Finance is not perfect, but its edited format usually gives readers more context and fewer emotional shortcuts.

| Feature | Kiplinger-style guidance | Online finance influencers |

|---|---|---|

| Main strength | Edited, researched, topic-based guidance | Fast, relatable, easy to watch |

| Best for | Taxes, retirement, insurance, Social Security, investing basics | Motivation, simple explainers, quick tips |

| Main risk | May not match every personal situation | Can be sponsored, biased, or oversimplified |

| Reader action | Use as a planning reference | Use as a starting point only |

| Best safety habit | Verify with official sources | Check credentials, conflicts, and evidence |

The smarter approach is not “old media vs new media.” It is using each format carefully. A short video may help you understand a concept quickly, but big decisions deserve more checking. The SEC’s Investor.gov warns investors to be careful with investment fraud red flags such as “risk-free” opportunities, guaranteed returns, aggressive sellers, and social media stock tips. That warning alone shows why edited guidance and official sources still matter.

Real-Life Examples for U.S. Readers

Imagine Linda, a 67-year-old retiree with Social Security, a traditional IRA, a Roth IRA, and a taxable brokerage account. Her biggest question is not “Which investment will make me rich?” Her real question is, “Which account should I withdraw from first, and how could taxes affect my Medicare premiums?” Kiplinger’s Personal Finance can help Linda understand withdrawal order, required minimum distributions, Social Security taxation, and why she may need a CPA or financial planner before making a major change.

Now picture Marcus, a 28-year-old worker who just got his first full-time job with a 401(k). He sees videos every day about hot stocks, crypto rebounds, and early retirement. But his first smart move may be simpler: understand his employer match, build an emergency fund, avoid high-interest credit card debt, and learn the difference between diversified funds and risky single-stock bets. Kiplinger’s Personal Finance gives Marcus a calmer way to learn investing without treating every market move like a sports match.

Consider a family earning $75,000 a year while rent, groceries, car insurance, and gas keep climbing. They may not need a complicated investment strategy this month. They may need a 30-day spending reset, a grocery limit, a debt payoff order, and a small emergency fund target. This is where your The Consumer Financial Protection Bureau also offers budgeting tools that can help households track income, bills, spending decisions, credit reports, and debt choices.

A homeowner has a different problem. Maybe property taxes increased, homeowners insurance is higher, and a roof repair is coming. Online advice may say “just refinance,” “just move,” or “just rent it out,” but that is too simple. A homeowner should compare local tax rules, insurance deductibles, cash reserves, home equity, and repair costs before making a decision. A careful money guide helps slow down the decision before it becomes an expensive mistake.

Who Should Read This in 2026?

Kiplinger’s Personal Finance is useful for readers who want organised money guidance without treating finance like entertainment. Here is how it helps different readers:

- Retirees: Use it for Social Security, withdrawal planning, taxes, estate planning, Medicare-related costs, and income strategies.

- Workers & Professionals: Use it to understand 401(k)s, IRAs, saving goals, investing basics, insurance choices, and employer benefits.

- Families: Use it for budgeting, college costs, inflation planning, home expenses, and protection against financial surprises.

Students and young adults can also benefit because early habits matter. A person who understands compounding, credit, taxes, risk, and budgeting in their 20s may avoid expensive mistakes later. Investors can use an established finance guide to understand market context, but they should still compare any idea with their own timeline and risk tolerance. The best reader is not someone looking for magic. The best reader is someone willing to learn, compare, verify, and act carefully.

What It Does Better Than Random Advice Online

The biggest advantage is context. Random online advice often answers the question that gets clicks, not the question that protects your money. Kiplinger’s Personal Finance tends to place a topic inside a broader financial picture. Retirement is not only about picking funds. It is also about taxes, withdrawal rates, health care, Social Security timing, inflation, longevity risk, and estate planning. Investing is not only about returns. It is also about risk, diversification, fees, behavior, and time horizon.

It also helps readers avoid emotional decisions. Markets rise and fall, tax rules change, headlines get dramatic, and influencers can make every issue sound urgent. A calmer editorial voice can remind readers to check the facts, run the numbers, and avoid all-or-nothing thinking. In personal finance, the boring middle is often where the wisdom lives.

Limitations of Kiplinger’s Personal Finance Readers Should Know

❌ What an Article Will Never Know About You

- Your True Numbers: Your exact income, current debt, and local state tax bracket.

- Your Real Life: Unexpected healthcare costs and unique family obligations.

- Your Mindset: Your exact current investment portfolio and true comfort taking risks.

🚨 6 Critical Decisions That Demand a Custom Plan

A generic article can explain the rules, but you should never put these six pillars on financial autopilot:

- Tax Planning: Customising strategies for your specific income level.

- Retirement Withdrawals: Knowing exactly which account to empty first to avoid penalties.

- Estate Documents: Legally protecting your wealth for the next generation.

- Insurance Coverage: Buying the right amount of shield without overpaying.

- Social Security Timing: Pinpointing the exact age to maximise your lifetime payouts.

- Large Investment Decisions: Deploying massive capital safely when the market shifts.

Readers should also remember that financial media can educate, but it should not become financial autopilot. Use articles to learn the language, understand trade-offs, and ask better questions. Then verify rules with official sources such as the IRS, Social Security Administration, Bureau of Labor Statistics, Consumer Financial Protection Bureau, and SEC Investor.gov. For personal decisions, a qualified tax professional, financial planner, attorney, or insurance specialist may be worth the cost.

Common Mistakes to Avoid

One common mistake is using one article as if it applies to everyone. A Roth IRA strategy that works for a 25-year-old may not fit a 62-year-old who is close to retirement. A high-yield savings account may be smart for emergency cash but not enough for long-term growth. A retirement withdrawal rule may be a helpful benchmark, but it still needs to be tested against taxes, market conditions, life expectancy, and spending needs.

Another mistake is trusting personality more than process. A confident creator can sound convincing, but confidence is not the same as accuracy. Before following any online money tip, make it a habit to ask yourself these four critical questions:

- 👤 Who wrote this? (Check the creator’s background and credentials)

- 📚 What source supports it? (Look for official data like IRS, SEC, or BLS)

- 🔍 Is there a conflict of interest? (See if it is a sponsored post or affiliate pitch)

- 🎯 Does it match my financial situation? (Ensure it fits your specific age, tax bracket, and goals) A careful finance resource can help readers build that habit of checking before acting.

Financial Disclaimer

This article is for educational and informational purposes only. It is not personal financial, investment, tax, legal, insurance, retirement, or estate planning advice. Every reader’s situation is different, and financial rules can change. Before making major money decisions, compare information with official sources and consider speaking with a qualified professional who understands your specific situation.

Conclusion

Kiplinger’s Personal Finance still matters in 2026 because Americans do not just need more money content; they need better filters. The internet gives readers speed, variety, personality, and convenience, but it can also create confusion. A trusted personal finance guide can slow things down, explain trade-offs, and help readers make decisions with more context.

Use it as a serious reference, not as a magic answer. Compare the guidance with your income, goals, debts, tax situation, insurance needs, and risk tolerance. Then use official sources and professional advice when the decision is big enough to affect your future. If you want more practical budgeting help, read my blog at https://financewithdevel.com/kiplingers-personal-finance-review/

FAQs

Is Kiplinger’s Personal Finance good for beginners?

Yes. It can help beginners understand investing, retirement accounts, taxes, saving, budgeting, insurance, and Social Security in simple language. Beginners should still compare what they read with official sources and their own financial situation.

Is Kiplinger’s Personal Finance only for retirees?

No. It covers retirement, but it also covers taxes, investing, saving, budgeting, insurance, real estate, college costs, and inflation. Workers, families, students, homeowners, and retirees can all find useful topics.

Can I rely on Kiplinger’s Personal Finance for investment decisions?

You can use it to understand investment ideas and market context, but do not rely on any article alone. Compare the information with your goals, risk tolerance, time horizon, and professional advice if needed.

How is it different from finance influencers?

Finance influencers are often faster and easier to watch, but their advice may be simplified, sponsored, or based on personal experience. Edited financial publications usually provide more context and source-backed explanations.

Should I still check official sources?

Yes. Always check official sources for rules, limits, deadlines, and government data. For example, use the IRS for retirement contribution limits, the SSA for Social Security information, BLS for inflation data, CFPB for consumer finance tools, and SEC Investor.gov for investment safety.

“Hi, I am Devel Gupta, an entrepreneur and the founder of FinanceWithDevel. With 10 years of experience in teaching and simplifying personal finance, my mission is to help beginners build long-term wealth without the confusing jargon. Whether it’s budgeting, investing, or retirement planning, I believe financial freedom starts with simple, consistent habits. Let’s make money make sense. Connect with me on [ LinkedIn/Twitter ] for more daily tips!”