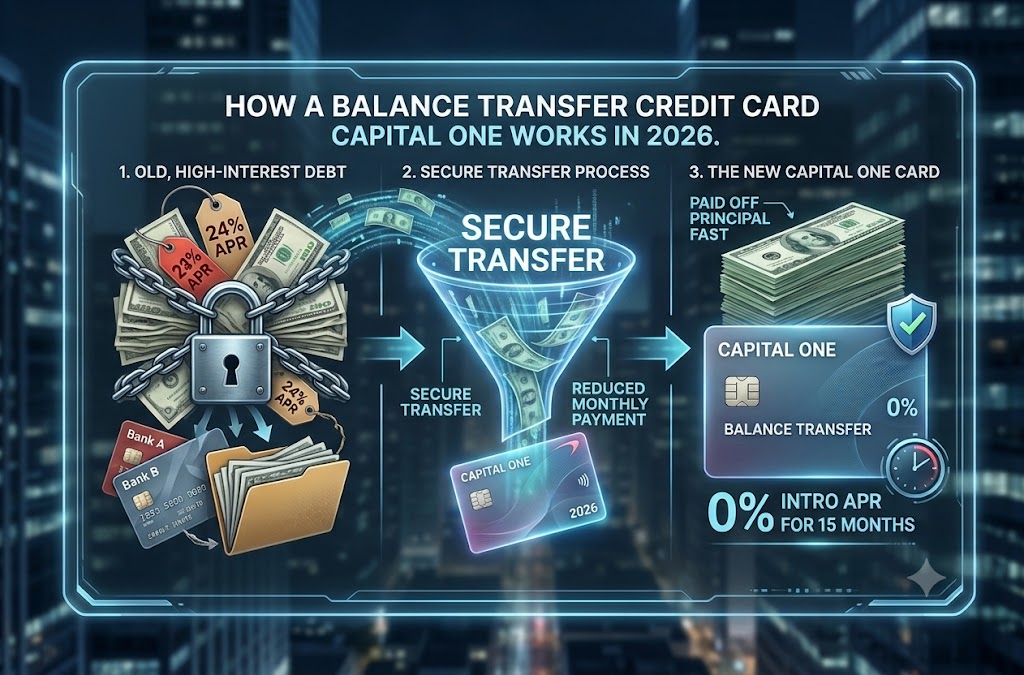

“If you want to save money on high-interest debt, a balance transfer credit card Capital One could be a great solution. A balance transfer lets you move debt from another creditor to a Capital One credit card, allowing you to pay less interest during the promotional period.”

After the transfer is completed, you make payments to Capital One instead of the old lender. However, you should keep paying the old card or loan until you confirm the transferred payment has been received. Missing a payment while the transfer is processing could lead to late fees or damage your credit.

A balance transfer is not the same as debt forgiveness. You still owe the money. The benefit is that a lower intro APR may allow more of your payment to go toward the principal balance rather than interest.

Who should consider a balance transfer credit card Capital One?

You may want to consider a balance transfer credit card Capital One if you have good or excellent credit, high-interest debt, and a realistic plan to pay off the transferred balance during the intro APR period. This option may also make sense if you are tired of juggling multiple payments and want to simplify your debt into one monthly payment.

It can be especially helpful for someone who is paying 20% or more APR on an existing credit card. In that case, even a balance transfer fee may be worth it if the intro APR gives you enough time to pay the debt down. The key is to calculate your monthly payment before applying. If you transfer $5,000 and have 15 months to pay it off, you should already know whether your budget can handle that payoff schedule.

Who should avoid it?

A balance transfer credit card Capital One may not be a good fit if you are only making minimum payments and do not have room in your budget to pay extra. It may also be a poor choice if the transfer fee is too high compared with your potential savings. If your balance is small or your current APR is already low, the math may not work in your favour.

You should also be careful if opening a new card might tempt you to spend more. A balance transfer can backfire if you move the old debt, free up the old card, and then start charging new purchases. That creates two balances instead of one. If your main issue is overspending, start with a budget and debt payoff plan before using another credit card.

Who Is This Card Best For?

A balance transfer credit card Capital One is best for borrowers who want a temporary interest break and have the discipline to pay down debt quickly. It may work well for people with strong credit, stable income, and a clear monthly payoff target. It can also help someone who wants a simple way to manage debt without taking out a personal loan.

It may also be useful for people who already understand credit card terms and are comfortable comparing APRs, balance transfer fees, and intro periods. The best users treat the intro period like a countdown clock. Every month matters.

Who Should Skip It?

A balance transfer credit card Capital One is not best for people who need long-term debt relief, cannot qualify for a strong offer, or may continue adding new debt. It may also not be ideal if another issuer offers a longer 0% intro APR period or a lower balance transfer fee.

It is also not the best option if you are close to missing payments or already struggling with basic monthly bills. In that situation, a nonprofit credit counseling agency or structured debt management plan may be safer than opening another credit card.

Capital One balance transfer comparison table

| Feature | What it means | Why it matters |

| Intro APR | A temporary low or 0% APR on eligible transfers | Helps reduce interest while you pay down debt |

| Intro period | The number of months the promotional APR lasts | A longer period gives you more time to repay |

| Regular APR | The APR after the intro period ends | Remaining balances may become costly |

| Balance transfer fee | A fee charged to move the balance | Reduces your total savings |

| Transfer eligibility | Rules on which debts can be moved | Capital One generally does not allow transfers between Capital One accounts |

| Credit limit | Your approved limit for purchases and transfers | Your transfer plus fee must fit within your eligible amount |

| Rewards | Cash back or miles on purchases | Balance transfers generally do not earn rewards |

How the Math Works

Let’s say you owe $5,000 on a credit card with a 24% APR. If you keep the balance on that card and pay it down slowly, interest can eat up a large part of your monthly payment. Now imagine you qualify for a balance transfer credit card Capital One with a 0% intro APR for 15 months.

Because balance transfer fees can vary by card and offer, use this as a sample calculation only. If the balance transfer fee were 3%, transferring $5,000 would cost $150, bringing your new balance to $5,150. To pay that off within 15 months, you would need to pay about $344 per month.

That may sound like a lot, but it gives you a clear target. If you can afford that payment, the transfer could help you avoid a meaningful amount of interest. If you cannot afford it, the remaining balance may face the regular variable APR after the intro period ends. That is why you should always run the numbers before applying.

Pros and cons of a balance transfer credit card Capital One

| Pros | Cons |

| May help reduce interest during the intro period | Balance transfer fee may apply |

| Can simplify debt into one payment | Intro APR does not last forever |

| More of your payment may go toward principal | Regular APR may be high after the promo ends |

| May help you pay debt faster with discipline | Approval and credit limit are not guaranteed |

| Some Capital One cards may have no annual fee | Balance transfers generally do not earn rewards |

What to check before applying

Before applying for a balance transfer credit card Capital One, check the latest APR, intro APR period, balance transfer fee, annual fee, credit score requirement, and transfer rules. Do not rely only on a blog summary, because card terms can change. Check the latest terms on Capital One’s official website before applying.

Also check whether the transfer must be completed within a specific time after account opening to qualify for the intro APR. Some card offers require transfers to be made within a certain window. If you miss that window, you may not receive the promotional rate.

Finally, compare Capital One with other balance transfer cards. A different issuer may offer a longer intro period or a lower transfer fee. The best card is not always the one with the most familiar name. It is the one that saves you the most money based on your real payoff plan.

Simple decision checklist

Before you apply, ask yourself:

- Can I qualify for the intro APR offer?

- How much is the balance transfer fee?

- Can I pay off the balance before the intro period ends?

- What APR applies after the intro period?

- Will I stop using the old card for new purchases?

- Have I checked the latest terms on Capital One’s official website before applying?

If the answer to most of these questions is yes, a balance transfer may be worth comparing. If not, slow down and review your budget first.

FAQs

What is a balance transfer credit card Capital One?

A balance transfer credit card Capital One is a Capital One credit card that may allow you to move debt from another creditor to Capital One. The goal is usually to take advantage of a low or 0% introductory APR and pay less interest while reducing the balance.

Can I transfer a balance from one Capital One card to another?

Generally, no. Capital One says you cannot transfer balances between two Capital One accounts. If you already have Capital One debt, check your options directly with Capital One.

Does a Capital One balance transfer earn rewards?

No. Capital One says balance transfers do not earn Capital One rewards. Rewards generally apply to eligible purchases, not transferred debt.

Is a balance transfer fee always charged?

A balance transfer fee may apply, depending on the card and offer. Because fees can change, check the latest pricing and terms on Capital One’s official website before applying.

What happens when the intro APR ends?

When the intro APR period ends, the regular variable APR may apply to any unpaid balance. That is why it is important to create a payoff plan before transferring debt.

Conclusion

A balance transfer credit card Capital One can be a smart option if you have high-interest debt, qualify for a strong intro APR offer, and have a realistic plan to pay the balance down. It can help lower interest costs, simplify payments, and give you a clear payoff window. But it is not right for everyone.

The smartest move is to compare the intro APR, regular APR, balance transfer fee, intro period, and transfer rules before applying. Do the math first. If the monthly payoff amount fits your budget, a balance transfer may help you move faster toward debt freedom. If the numbers do not work, consider other debt payoff options before opening a new card.

Financial disclaimer: This article is for educational purposes only and does not recommend one credit card over another. Credit card terms, APRs, fees, and promotional offers can change. Check the latest terms on Capital One’s official website before applying and consider speaking with a qualified financial professional if you need personalised advice.

“Hi, I am Devel Gupta, an entrepreneur and the founder of FinanceWithDevel. With 10 years of experience in teaching and simplifying personal finance, my mission is to help beginners build long-term wealth without the confusing jargon. Whether it’s budgeting, investing, or retirement planning, I believe financial freedom starts with simple, consistent habits. Let’s make money make sense. Connect with me on [ LinkedIn/Twitter ] for more daily tips!”