What Is the 50/30/20 Budget Rule?

50/30/20 Budget Rule Explained simply means dividing your after-tax income into three easy buckets: 50% for needs, 30% for wants, and 20% for savings or debt repayment. Instead of tracking every tiny expense like a detective with a magnifying glass, this rule gives you a clean money map. Think of it like a traffic signal for your income: needs get the green light first, wants get a controlled yellow light, and savings get a protected lane so your future does not get stuck in traffic. The beauty of this rule is that it feels realistic because it does not ask you to stop living your life. You can still eat out, watch movies, buy coffee, travel sometimes, and enjoy your money, but you also create structure so your paycheck does not vanish like magic by the 20th of the month.

50/30/20 Budget Rule Explained is especially useful for beginners because most people fail at budgeting when the system is too strict. A budget that says “never spend on fun” usually collapses faster than a cheap umbrella in heavy rain. This rule understands that money is emotional, social, and practical at the same time. You need rent, groceries, utilities, transport, insurance, and minimum loan payments, but you also need small joys. At the same time, you cannot ignore emergency savings, retirement contributions, investments, or high-interest debt. That is why this method works like a balanced plate: half goes to essentials, some portion goes to lifestyle, and a meaningful part goes to future security.

Why This Budget Rule Still Works Today

50/30/20 Budget Rule Explained matters even more today because many households are dealing with higher living costs, job uncertainty, and pressure to spend. According to the Federal Reserve’s 2025 household well-being findings, 73% of U.S. adults said they were either doing okay financially or living comfortably, but price increases remained the most common financial concern, with just above 9 in 10 adults saying price increases were at least a minor or major concern. The same report said 63% of adults could cover a hypothetical $400 emergency using cash, savings, or a credit card paid off at the next statement, which means a large share of people still feel financially fragile when surprise expenses arrive.

This is where 50/30/20 Budget Rule Explained becomes practical, not just theoretical. When prices rise, people often try random cost-cutting: cancel this, reduce that, panic for two weeks, then return to old habits. A better approach is to create a repeatable system. The rule helps you quickly see whether your housing, car payment, food spending, subscriptions, shopping, and debt are fighting each other. If your needs already take 70% of your income, the problem is not your coffee; the problem is that your fixed expenses are too heavy. If your wants are quietly eating 45%, the issue may be lifestyle creep. If savings are always “whatever is left,” then the future is getting leftovers, and honestly, your future self deserves a better meal.

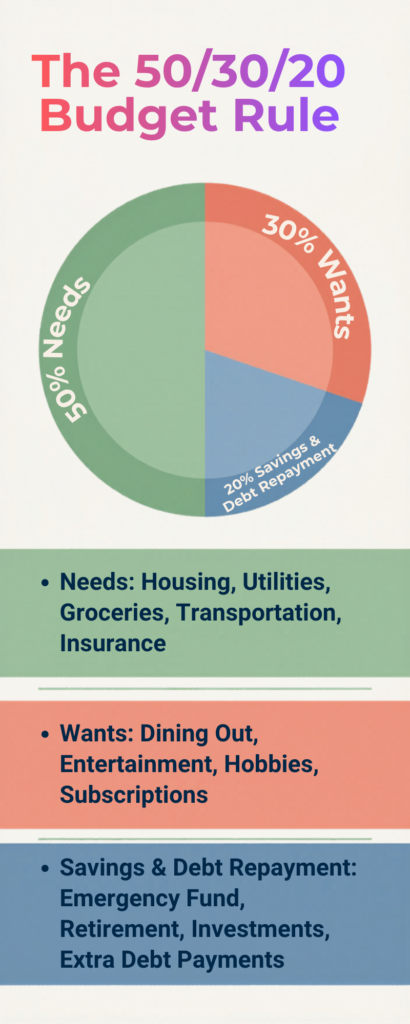

How the 50/30/20 Formula Breaks Down

50/30/20 Budget Rule Explained starts with after-tax income, not your gross salary. That means you should use the amount that actually reaches your bank account after taxes and mandatory deductions. This is important because many people make a budget based on their full salary and then wonder why the math feels cursed. If your monthly take-home income is $4,000, the rule suggests $2,000 for needs, $1,200 for wants, and $800 for savings or debt repayment. It is simple enough to remember, but flexible enough to adjust when life gets complicated.

Here is the basic structure:

| Budget Category | Percentage | Purpose |

|---|---|---|

| Needs | 50% | Rent, groceries, utilities, transport, insurance, minimum debt payments |

| Wants | 30% | Dining out, shopping, entertainment, travel, subscriptions |

| Savings and Debt | 20% | Emergency fund, investments, retirement, extra debt payments |

The reason 50/30/20 Budget Rule Explained works well is that it separates survival, enjoyment, and progress. If you mix all three together, every expense feels equally important. Suddenly, a streaming subscription, rent payment, and emergency fund contribution all compete in the same mental basket. That creates confusion. But when you classify expenses clearly, you get control without needing a complicated spreadsheet. You can look at your spending and ask: “Is this a need, a want, or future-building?” That one question alone can save you from many unnecessary purchases.

50% for Needs

In 50/30/20 Budget Rule Explained, needs are the expenses you must pay to live, work, and stay financially stable. These usually include rent or mortgage payments, groceries, basic utilities, transportation, health insurance, minimum debt payments, and essential phone or internet costs. Needs are not always exciting, but they are the foundation of your financial house. If this part is weak, the whole structure shakes. The problem is that many people accidentally allow wants to disguise themselves as needs. For example, basic groceries are a need, but daily premium food delivery is usually a want. A basic phone plan may be a need, but the most expensive plan with features you never use may be a want wearing a fake mustache.

50/30/20 Budget Rule Explained becomes powerful when you honestly audit this 50% category. U.S. Bureau of Labor Statistics data shows how heavy essential costs can become: in 2024, average annual household spending was $78,535, or about $6,545 per month, and housing plus transportation together accounted for more than 50% of total spending. Housing alone averaged $26,266 per year, while transportation averaged $13,318 per year. That tells us something important: for many households, the biggest budget wins do not come from tiny cuts; they come from managing rent, mortgage, car costs, commuting, insurance, and food routines. If your needs are above 50%, you may still use this rule, but you will need a realistic adjustment plan instead of feeling guilty every month.

30% for Wants

50/30/20 Budget Rule Explained does not punish you for enjoying life. The 30% wants category is what makes the rule sustainable. Wants include restaurants, coffee shops, movies, hobbies, streaming services, gym upgrades, travel, shopping, gifts, and other lifestyle expenses. This is the part of the budget that keeps you from feeling like you are living inside a financial prison. Cutting every want may look smart on paper, but in real life it often leads to frustration spending. You behave strictly for two weeks, then one bad day comes, and suddenly your cart is full, your wallet is crying, and your budget is pretending it never knew you.

The smart way to use 50/30/20 Budget Rule Explained is not to remove wants; it is to prioritize them. You can ask yourself, “Which wants actually make my life better?” Maybe travel gives you joy, but random online shopping does not. Maybe a gym membership improves your health, but five unused subscriptions quietly drain money. Maybe eating out with friends matters, but ordering expensive delivery out of laziness does not. Wants should feel intentional, not automatic. This category gives you permission to spend, but with boundaries. That is the sweet spot: you enjoy your present without robbing your future.

20% for Savings and Debt Repayment

The 20% category in 50/30/20 Budget Rule Explained is where your financial future gets built. This bucket can include emergency savings, retirement contributions, investing, extra loan payments, credit card debt payoff, and other long-term goals. If needs keep you alive and wants keep life enjoyable, this category keeps you from being trapped. It is your escape ladder from paycheck-to-paycheck stress. Even small savings matter because money saved consistently becomes a shield. It protects you from medical bills, car repairs, job loss, business slowdowns, and all the annoying surprises life throws like a mischievous cricket bowler.

50/30/20 Budget Rule Explained also fits well with emergency fund advice. The Consumer Financial Protection Bureau says the amount needed in an emergency fund depends on your personal situation, past unexpected expenses, and cash-flow pattern, and it recommends creating savings goals, making consistent contributions, monitoring progress, and automating savings where possible. Bankrate also notes that many experts suggest keeping three to six months of living expenses in an emergency fund, while its latest emergency savings reporting found that only 46% of U.S. adults had enough to cover three months of expenses and 24% had no emergency savings at all. This is exactly why the 20% bucket should not be treated as optional. It is not “extra money”; it is your financial oxygen tank.

Why People Feel Broke Even When They Earn Well

50/30/20 Budget Rule Explained also helps answer a painful question: why do some people earn decent money but still feel broke? The answer is usually not one big mistake. It is often a collection of small leaks. Higher income can quietly invite bigger rent, a better car, more subscriptions, premium food delivery, impulse shopping, expensive weekends, and “I deserve it” purchases. And yes, you may deserve comfort, but your bank account also deserves breathing space. Lifestyle creep is sneaky because every upgrade feels reasonable in isolation. One subscription is fine. One dinner is fine. One EMI is fine. But together, they turn your paycheck into a crowded train with no seat left for savings.

When 50/30/20 Budget Rule Explained is applied honestly, it reveals the truth without drama. If your income rises but your savings rate stays flat, your lifestyle has swallowed the raise. If your needs are too high, you are financially locked before the month begins. If your wants are too high, you may be using spending as stress relief. If your 20% savings bucket is empty, every emergency becomes a crisis. Feeling broke is not always about low income; sometimes it is about unclear allocation. This rule gives every rupee, dollar, or euro a job before it disappears into random spending fog.

A Simple 50/30/20 Budget Example

Let’s make 50/30/20 Budget Rule Explained easy with a monthly take-home income example. Suppose you earn $4,000 after tax every month. Under this rule, $2,000 goes to needs, $1,200 goes to wants, and $800 goes to savings or extra debt payments. If you earn $2,500 after tax, then $1,250 goes to needs, $750 goes to wants, and $500 goes to savings or debt. If you earn $6,000 after tax, then $3,000 goes to needs, $1,800 goes to wants, and $1,200 goes to savings or debt. The math is simple, but the discipline comes from checking whether your real spending matches the target.

| Monthly Take-Home Income | Needs 50% | Wants 30% | Savings/Debt 20% |

|---|---|---|---|

| $2,500 | $1,250 | $750 | $500 |

| $4,000 | $2,000 | $1,200 | $800 |

| $6,000 | $3,000 | $1,800 | $1,200 |

| $8,000 | $4,000 | $2,400 | $1,600 |

The best part of 50/30/20 Budget Rule Explained is that it can show you the gap between your ideal budget and your real budget. For example, if your take-home income is $4,000 but your needs are $2,700, you are already at 67.5% before wants and savings. That does not mean you are bad with money. It means your fixed expenses need attention. Maybe rent is too high, transportation is expensive, groceries are unplanned, or insurance and debt payments are squeezing you. Once you know the real issue, you can solve the right problem instead of blaming yourself for everything.

How to Use the Rule Without Feeling Restricted

50/30/20 Budget Rule Explained should feel like a guide, not a punishment. The easiest way to make it work is to automate your savings first. When your income arrives, move the 20% savings or debt amount immediately to a separate account, investment account, or loan repayment plan. This prevents the classic mistake of saving whatever remains at the end of the month. Let’s be honest: money left in the main account often behaves like snacks left on the table—it disappears. Automation removes daily willpower from the process. You do not need to feel motivated every day; the system quietly does the work.

Another way to make 50/30/20 Budget Rule Explained feel easier is to reduce invisible spending instead of cutting things you love. Invisible spending includes unused subscriptions, bank fees, insurance overpayment, random delivery charges, unplanned app purchases, and small convenience costs that repeat too often. These expenses are boring, which is exactly why they are dangerous. They do not give you a memorable experience, but they still reduce your savings. Start by checking your last 60 days of transactions. Circle anything you forgot you were paying for. If an expense gives low joy and repeats monthly, it is a perfect target.

Keep Enjoyment in the Budget

A major reason 50/30/20 Budget Rule Explained works better than extreme budgeting is that it protects guilt-free spending. You should not feel bad for buying something fun when it fits inside your wants category. In fact, planned enjoyment can reduce impulse spending because your brain does not feel starved. If you enjoy eating out, keep a restaurant budget. If you love books, keep a book budget. If travel motivates you, create a travel fund. The goal is not to become a money robot. The goal is to spend on purpose.

This is where 50/30/20 Budget Rule Explained becomes emotionally smart. Money is not only numbers; it is mood, identity, confidence, pressure, and habits. When a budget is too harsh, people rebel against it. When a budget is too loose, money leaks everywhere. This rule sits in the middle. You get structure and freedom together. You can enjoy the present while still building an emergency fund, reducing debt, and investing for the future. That balance is what helps you save more without feeling broke.

Common Mistakes to Avoid

The biggest mistake with 50/30/20 Budget Rule Explained is misclassifying wants as needs. A need is something essential for basic living and work. A want is something that improves comfort, status, convenience, or enjoyment. There is nothing wrong with wants, but calling them needs hides the real picture. Another common mistake is using gross salary instead of take-home income. If you calculate from gross income, your budget will look better than reality, and then you will wonder why the plan does not work. Always use after-tax income.

Another mistake in 50/30/20 Budget Rule Explained is ignoring debt interest. Minimum debt payments usually belong in needs because you must pay them, but extra debt payments belong in the 20% savings and debt category. If you have high-interest credit card debt, paying it down can be more urgent than investing because the interest cost may be eating your progress. People also make the mistake of trying to perfect the budget from day one. Don’t do that. Your first month is a diagnosis. Your second month is improvement. Your third month is where the system starts becoming natural.

When the 50/30/20 Rule Needs Adjustment

50/30/20 Budget Rule Explained is a strong starting point, but it is not a law carved into stone. If you live in a high-cost city, your needs may be above 50%. If you are aggressively paying debt, your savings/debt category may need to be more than 20%. If you are a student, freelancer, business owner, or someone with irregular income, you may need a slightly different version. For example, a 60/20/20 budget may work temporarily if rent and food are high. A 50/20/30 version may work if you are young and focusing heavily on savings. A 70/20/10 plan may be realistic for someone with very low income and high fixed expenses.

The flexible mindset behind 50/30/20 Budget Rule Explained is more important than the exact percentages. The rule teaches you to separate expenses into needs, wants, and future-building. Once you understand that structure, you can adjust the ratio without losing control. But be careful: adjustment should be based on reality, not excuses. If needs are 65% because rent is genuinely high, that is different from needs being 65% because every comfort has been renamed as essential. Your budget should challenge you gently, not crush you. Like a good fitness plan, it should stretch your habits without making you quit.

Best Tools to Track This Budget

You can apply 50/30/20 Budget Rule Explained with a notebook, spreadsheet, budgeting app, or even three separate bank accounts. The tool matters less than consistency. If you like simplicity, create three labels in your spreadsheet: needs, wants, savings/debt. At the end of each week, add your expenses under each label. If you prefer automation, use a budgeting app or your bank’s spending tracker. If you struggle with overspending, separate accounts can help. Keep one account for bills, one for spending, and one for savings. This creates physical distance between your future money and your shopping mood.

For beginners, the easiest version of 50/30/20 Budget Rule Explained is the weekly check-in method. Every Sunday, review your spending for 10 minutes. Ask three questions: Did my needs stay close to 50%? Did my wants stay close to 30%? Did I protect my 20% savings or debt goal? This short weekly review is better than a dramatic monthly panic session. When you catch overspending early, you can adjust calmly. When you ignore it for 30 days, the budget starts looking like a crime scene. Small reviews create big control.

Conclusion

50/30/20 Budget Rule Explained is not about becoming cheap, boring, or scared of spending. It is about giving your money a clear direction so you can save more without feeling broke. The rule works because it accepts real life: you have bills, you have dreams, and you also want to enjoy today. By placing 50% toward needs, 30% toward wants, and 20% toward savings or debt repayment, you create a balanced system that is simple enough to follow and strong enough to change your financial life. The magic is not in the percentages alone; the magic is in awareness, consistency, and honest choices.

If your current budget does not match the rule perfectly, do not panic. Start where you are. Track your spending for one month, identify the biggest leaks, automate a small savings amount, and slowly move closer to the 50/30/20 structure. 50/30/20 Budget Rule Explained gives you a practical path, not a perfect test. You do not need to feel deprived to build wealth. You need a system that protects your needs, gives room for joy, and pays your future self first. That is how saving becomes less painful and more powerful.

FAQs

1. What is the 50/30/20 budget rule in simple words?

The 50/30/20 budget rule means you divide your after-tax income into three parts: 50% for needs, 30% for wants, and 20% for savings or debt repayment. Needs include rent, groceries, transport, utilities, and minimum debt payments. Wants include restaurants, shopping, entertainment, travel, and subscriptions. Savings include emergency funds, investing, retirement contributions, and extra loan payments. It is popular because it is simple, flexible, and easier to follow than a strict line-by-line budget.

2. Is the 50/30/20 rule good for beginners?

Yes, it is one of the best budgeting methods for beginners because it does not require complicated tracking. A beginner can start by calculating take-home income and then dividing expenses into three broad groups. This makes money management less stressful and more visual. It also helps beginners quickly identify whether they are overspending on needs, wants, or ignoring savings. The rule is not perfect for every situation, but it is a strong starting point.

3. What if my needs are more than 50%?

If your needs are more than 50%, first check whether all those expenses are truly needs. Sometimes expensive habits hide inside the needs category. If they are genuine needs, such as rent, groceries, transport, and insurance, then adjust the rule temporarily. You may use 60/20/20 or 70/20/10 until your income rises or fixed expenses reduce. The goal is progress, not perfection.

4. Should debt repayment be included in the 20% category?

Minimum debt payments usually belong in the needs category because they are required payments. Extra debt repayment belongs in the 20% savings and debt category. If you have high-interest credit card debt, extra repayment may be more urgent than investing because interest can grow quickly. Once expensive debt is reduced, you can redirect more of that 20% toward emergency savings, retirement, or investments.

5. Can I use the 50/30/20 rule with irregular income?

Yes, but you should use your average monthly income or your lowest expected monthly income as the base. If your income changes every month, build a buffer account first so your bills stay stable. During high-income months, save more than 20% if possible. During low-income months, protect essentials and avoid unnecessary debt. The rule still works, but irregular income requires more cash-flow planning.

Read more beginner-friendly finance guides on “our blog” financewithdevel.com

“Hi, I am Devel Gupta, an entrepreneur and the founder of FinanceWithDevel. With 10 years of experience in teaching and simplifying personal finance, my mission is to help beginners build long-term wealth without the confusing jargon. Whether it’s budgeting, investing, or retirement planning, I believe financial freedom starts with simple, consistent habits. Let’s make money make sense. Connect with me on [ LinkedIn/Twitter ] for more daily tips!”