A Solo 401(k) is a retirement plan designed for self-employed people, freelancers, consultants, independent contractors, and small business owners who do not have full-time employees other than a spouse. Think of it like a regular 401(k), but built for one-person businesses. The main reason people love it is simple: you can contribute as both the employee and the employer. That dual role is what makes the Solo 401(k) Contribution Limits 2026 so powerful compared with many other retirement accounts.

You can also read the IRS one-participant 401(k) plan rules to understand the official requirements before opening a Solo 401(k).

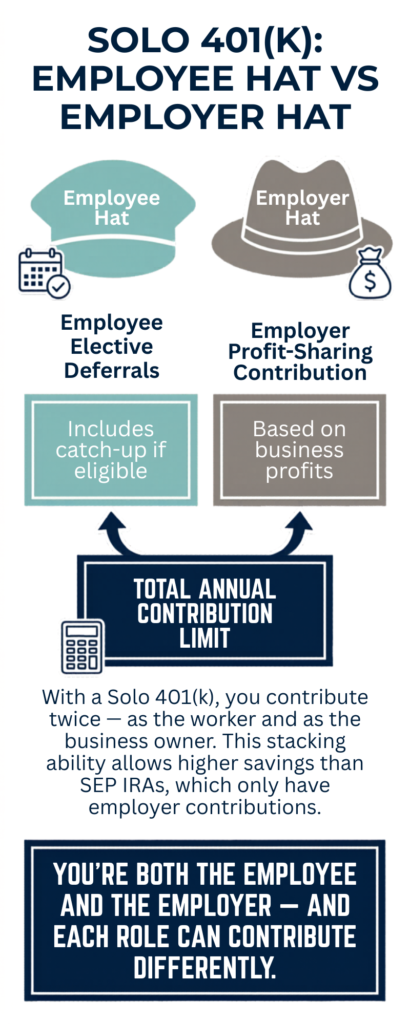

The IRS describes a one-participant 401(k) plan as a plan where the business owner can contribute in two capacities: as an employee through elective deferrals and as an employer through nonelective contributions. The IRS even explains that the business owner “wears two hats,” which is the easiest way to understand the plan.

For freelancers, this plan can feel like a financial upgrade button. Instead of saving only a small IRA amount, you may be able to put away much more money if your business income supports it. That is why Solo 401(k) Contribution Limits 2026 matter so much for designers, consultants, coaches, YouTubers, writers, real estate agents, online sellers, and independent professionals.

Why Freelancers and Business Owners Use It

Freelancers and business owners usually deal with irregular income. Some months feel amazing, while other months feel like your bank account is doing yoga in survival mode. A Solo 401(k) helps because it gives flexibility. You are not forced to contribute the same amount every month, and you can plan contributions based on actual business profit.

The second big benefit is tax planning. Traditional Solo 401(k) contributions may reduce taxable income now, while Roth Solo 401(k) contributions may help create tax-free retirement withdrawals later if the rules are followed. This makes Solo 401(k) Contribution Limits 2026 more than just a number; they become a planning tool. A freelancer earning strong income in 2026 can use the plan to build retirement wealth and potentially manage taxes at the same time.

Solo 401(k) Contribution Limits 2026 at a Glance

For 2026, the employee elective deferral limit for 401(k), 403(b), most 457 plans, and the federal Thrift Savings Plan increased to $24,500, up from $23,500 in 2025, according to the IRS. The overall defined contribution limit under section 415(c) increased to $72,000 for 2026, not counting catch-up contributions.

Here is the clean view of Solo 401(k) Contribution Limits 2026:

| Contribution Type | 2026 Limit |

|---|---|

| Employee elective deferral | $24,500 |

| Catch-up contribution, age 50+ | $8,000 |

| Super catch-up, age 60–63 | $11,250 |

| Total employee + employer limit, under age 50 | $72,000 |

| Total with standard catch-up, age 50+ | $80,000 |

| Total with super catch-up, age 60–63 | $83,250 |

| Annual compensation limit | $360,000 |

official IRS 2026 retirement contribution limits

This table is the core of Solo 401(k) Contribution Limits 2026. But don’t just look at the biggest number and assume everyone can contribute that much. Your real limit depends on your business income, business structure, age, and whether you also contribute to another workplace 401(k).

Employee Contribution Limit

The employee side is the easier part. In 2026, you can contribute up to $24,500 as an employee elective deferral, or 100% of your eligible compensation if your compensation is lower. This limit applies across 401(k)-type plans, not separately to every plan you own. So, if you have a regular job with a 401(k) and also run a side business with a Solo 401(k), your employee deferrals across both plans generally share the same annual limit.

This is where many people make mistakes. They think, “I have two plans, so I get two employee limits.” Not quite. The IRS says the basic elective deferral limit is $24,500 in 2026, or 100% of compensation, whichever is less. That means Solo 401(k) Contribution Limits 2026 must be planned together with any other 401(k), 403(b), SIMPLE, or similar salary deferral you may already use.

Employer Contribution Limit

The employer side is where the Solo 401(k) becomes especially useful. As the employer, your business can make profit-sharing or nonelective contributions. For corporations, employer contributions are generally up to 25% of compensation. For self-employed individuals, the calculation is more technical because your “earned income” is reduced by one-half of self-employment tax and the contribution for yourself. The IRS specifically says self-employed individuals must make a special computation for maximum elective deferrals and nonelective contributions.

In simple language, sole proprietors often hear the shortcut: employer contribution is roughly 20% of adjusted net self-employment income. For S-corp owners, it is often based on W-2 wages, not total business profit. That is why Solo 401(k) Contribution Limits 2026 should not be calculated casually on a napkin. The plan is powerful, but the math needs to be clean.

Total Contribution Limit

The total 2026 limit for employee plus employer contributions is $72,000 for people under age 50. Catch-up contributions can go above that number. So, if you are age 50 or older, your total could reach $80,000 with the standard $8,000 catch-up. If you are age 60 to 63 and your plan allows the higher catch-up, your total could reach $83,250.

This is the headline reason Solo 401(k) Contribution Limits 2026 are attractive. A high-earning freelancer or owner-only business can potentially save far more than with a traditional IRA. But remember, the limit is not a promise. It is a ceiling. Your income must support the contribution, and your plan document must allow the contribution type you want.

2026 Catch-Up Contribution Rules

Catch-up contributions are extra retirement contributions available to older savers. For 2026, the standard 401(k) catch-up contribution for people age 50 and older is $8,000, according to the IRS. The SECURE 2.0 higher catch-up rule also applies for ages 60, 61, 62, and 63, and for 2026 that higher catch-up remains $11,250.

This means Solo 401(k) Contribution Limits 2026 become even stronger for people who started late or want to accelerate retirement savings in their 50s and early 60s. It is like getting a bigger bucket when you are closer to the finish line.

Age 50 and Older Catch-Up

If you are 50 or older by the end of 2026, you may be able to contribute an extra $8,000 as a catch-up contribution. This can bring your employee contribution total to $32,500: the regular $24,500 limit plus the $8,000 catch-up. For many business owners, this is a big deal because retirement planning often becomes more serious in the 50s.

At this stage, people usually have clearer goals. Maybe the mortgage is lower. Maybe kids are older. Maybe business income is stronger. That is when Solo 401(k) Contribution Limits 2026 can help convert peak earning years into long-term wealth.

Age 60 to 63 Super Catch-Up

For ages 60 to 63, the 2026 higher catch-up limit is $11,250 instead of the standard $8,000. That can bring the employee contribution amount to $35,750 before employer contributions are added. The IRS confirms that the higher catch-up contribution limit for employees aged 60 through 63 remains $11,250 for 2026.

This super catch-up is especially useful for business owners who had uneven income earlier in life. Maybe you spent years building your company, reinvesting profits, or handling family expenses. Solo 401(k) Contribution Limits 2026 give you a chance to push harder during the years when retirement is no longer far away.

How Solo 401(k) Contributions Work

A Solo 401(k) contribution is not one single bucket. It has two main parts: employee deferral and employer contribution. The employee deferral can be traditional pre-tax, Roth if your plan allows it, or a mix of both. The employer contribution is generally pre-tax and comes from the business side. Together, these create the total annual contribution.

The magic of Solo 401(k) Contribution Limits 2026 is that you can use both roles. A regular employee usually depends on an employer match or profit-sharing formula. But as a solo business owner, you control both sides, subject to IRS rules. That is why this plan is often better for high-saving self-employed people than simpler plans.

Employee Hat vs Employer Hat

Imagine you own a small coffee shop, and you are also the barista. One moment, you are the worker making coffee. The next moment, you are the owner checking profit. A Solo 401(k) works in a similar way. You contribute first as the worker, then your business can contribute as the owner.

This “two hats” idea makes Solo 401(k) Contribution Limits 2026 easier to understand. The employee hat gives you the $24,500 elective deferral limit. The employer hat may allow additional profit-sharing contributions, depending on income. But both hats still live under the same IRS roof, so the combined annual limit matters.

Sole Proprietor vs S-Corp Calculation

For a sole proprietor or single-member LLC taxed as a sole proprietorship, contributions are usually based on net earnings from self-employment after adjustments. The employer portion is not simply 25% of Schedule C profit, because self-employment tax and the contribution itself affect the calculation. This is why tax software or a CPA can be valuable.

For an S-corp owner, the calculation usually starts with reasonable W-2 wages paid to the owner. Employer contributions are generally based on those wages, not total distributions. So if an S-corp owner pays themselves very low wages and takes large distributions, Solo 401(k) Contribution Limits 2026 may not be as high as expected.

Traditional vs Roth Solo 401(k)

A traditional Solo 401(k) contribution may reduce taxable income now, which can be useful if you are in a high tax bracket. A Roth Solo 401(k) contribution does not reduce today’s taxable income, but qualified withdrawals may be tax-free later. The right choice depends on whether you expect your tax rate to be higher now or in retirement.

For 2026 planning, Roth features are worth paying attention to because SECURE 2.0 introduced Roth catch-up rules for certain higher-income workers. The IRS announced final regulations in 2025 stating that Roth catch-up provisions generally apply to contributions in taxable years beginning after December 31, 2026.

For freelancers and business owners, Solo 401(k) Contribution Limits 2026 should be viewed through both contribution limits and tax strategy. Pre-tax is not automatically better. Roth is not automatically better. The smarter move is the one that fits your current income, future tax expectations, and cash-flow comfort.

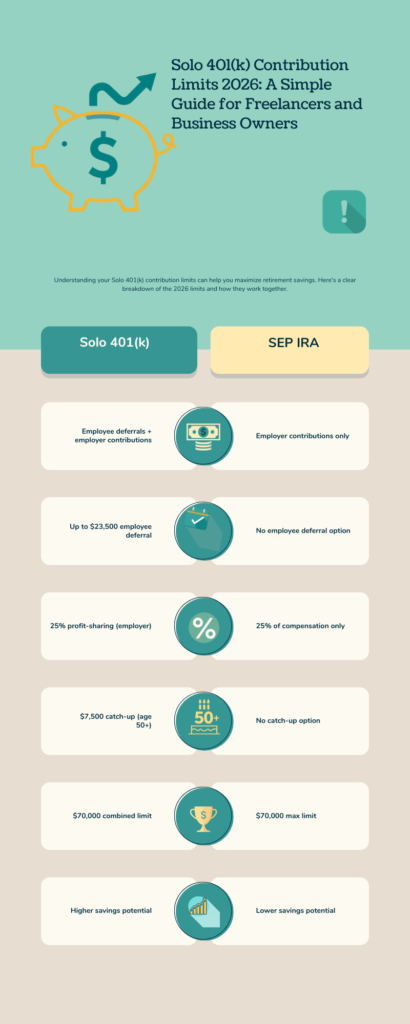

Solo 401(k) vs SEP IRA

A SEP IRA is simpler, but a Solo 401(k) can allow higher contributions at lower income levels because it includes employee deferrals. With a SEP IRA, contributions are employer-only. With a Solo 401(k), you may contribute as both employee and employer. That difference can matter a lot for freelancers earning moderate income.

If you are still confused between both retirement plans, read this detailed comparison: Solo 401(k) vs SEP IRA in 2026

| Feature | Solo 401(k) | SEP IRA |

|---|---|---|

| Employee deferral allowed | Yes | No |

| Roth option possible | Yes, if plan allows | Usually no traditional SEP Roth structure unless specific rules/provider allow |

| Catch-up contributions | Yes | No |

| Best for | Owner-only businesses wanting high savings flexibility | Simple employer-only retirement saving |

| Complexity | Moderate | Lower |

This is why Solo 401(k) Contribution Limits 2026 are often more attractive for solo owners than SEP IRA limits. A freelancer earning $80,000, for example, may be able to save more with a Solo 401(k) than with a SEP IRA because the employee deferral comes first.

Common Mistakes to Avoid

The first common mistake is overcontributing. This can happen when someone has a day job 401(k) and a Solo 401(k). Remember, the employee deferral limit is shared across plans. If you already contributed $15,000 at your job, you do not get a fresh $24,500 employee limit for your business plan.

The second mistake is ignoring the employer contribution calculation. Many self-employed people assume they can contribute 25% of business profit, but the IRS calculation for self-employed individuals is more detailed.

The third mistake is forgetting Form 5500-EZ. The IRS says a one-participant 401(k) plan is generally required to file Form 5500-EZ if it has $250,000 or more in assets at the end of the year.

The fourth mistake is setting up the plan too late. Deadlines can depend on business type and contribution type, so it is better to plan early. Solo 401(k) Contribution Limits 2026 are useful only if the plan is properly opened, funded, and documented.

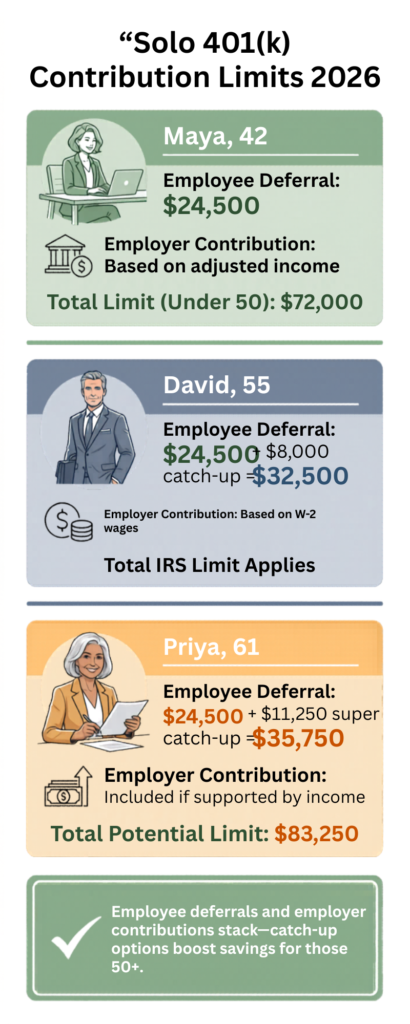

Simple Example for 2026

Let’s say Maya is a 42-year-old freelance consultant with strong net self-employment income in 2026. She wants to save aggressively. She may be able to contribute up to $24,500 as an employee deferral. Then she may add an employer contribution based on her adjusted self-employment income. Her total employee plus employer contribution cannot exceed $72,000 because she is under 50.

Now imagine David is 55 and owns an S-corp. He pays himself W-2 wages and wants to maximize retirement saving. He may contribute up to $24,500 as an employee, plus the $8,000 catch-up, making his employee-side total $32,500. His company may also make an employer contribution based on eligible compensation, but the total must follow the IRS limits.

Now consider Priya, age 61. If her plan allows the super catch-up, her employee-side contribution can reach $35,750 in 2026: $24,500 plus $11,250. With employer contributions added, her total may reach $83,250 if income supports it. This is the most powerful version of Solo 401(k) Contribution Limits 2026.

Who Should Consider a Solo 401(k)?

A Solo 401(k) may be a strong fit if you are self-employed with no full-time employees, want to save more than an IRA allows, and have enough business income to support meaningful contributions. It may also suit people with side businesses, especially if they want employer-side contributions after using a workplace 401(k). The plan is flexible, powerful, and built for people who want more control.

However, it is not perfect for everyone. If your income is very low or irregular, an IRA may be simpler. If you plan to hire employees soon, a Solo 401(k) may create more compliance responsibilities. If you dislike paperwork, a SEP IRA may feel easier. Still, for many freelancers and owner-only businesses, Solo 401(k) Contribution Limits 2026 offer one of the best retirement-saving opportunities available.

Final Planning Tips for 2026

Start by estimating your 2026 business income. Then decide how much cash you can comfortably save without hurting your business operations. Retirement saving is important, but your business still needs fuel. Do not drain your working capital just to hit a contribution number.

Next, decide between traditional and Roth contributions. If your income is high in 2026, traditional contributions may reduce current taxable income. If your tax rate is lower now or you want tax-free retirement income later, Roth may be attractive. Then review whether your plan allows Roth, loans, after-tax contributions, and catch-up contributions.

Also, coordinate with your CPA or tax professional. Solo 401(k) Contribution Limits 2026 involve IRS rules, business structure, self-employment tax, compensation limits, and deadlines. A small mistake can create unnecessary stress. A good calculation upfront can save you from correction work later.

Conclusion

Solo 401(k) Contribution Limits 2026 give freelancers and business owners a serious opportunity to build retirement wealth. The employee deferral limit is $24,500, the standard catch-up for age 50+ is $8,000, the super catch-up for ages 60 to 63 is $11,250, and the total employee plus employer limit is $72,000 before catch-up contributions. For the right person, this plan can be much more powerful than a basic IRA.

The best way to use a Solo 401(k) is not to chase the maximum blindly. Instead, match your contribution to your income, tax situation, business structure, and long-term goals. If your business is doing well, Solo 401(k) Contribution Limits 2026 can help you turn today’s profit into tomorrow’s financial freedom.

FAQs

1. What are the Solo 401(k) Contribution Limits 2026?

The main Solo 401(k) Contribution Limits 2026 are $24,500 for employee elective deferrals and $72,000 for total employee plus employer contributions before catch-up contributions. If you are age 50 or older, you may add a catch-up contribution of $8,000. If you are age 60 to 63, the higher catch-up contribution may be $11,250 if your plan allows it.

2. Can I contribute to a Solo 401(k) if I also have a job?

Yes, you can have a Solo 401(k) for self-employment income even if you also have a regular job. But your employee elective deferral limit is shared across 401(k)-type plans. So, Solo 401(k) Contribution Limits 2026 must be coordinated with your workplace 401(k).

3. Is the $72,000 limit guaranteed for everyone?

No. The $72,000 number is the maximum combined employee and employer limit before catch-up contributions. Your actual limit depends on eligible compensation, business income, and plan rules. That is why Solo 401(k) Contribution Limits 2026 should be calculated based on your real numbers.

4. Is a Solo 401(k) better than a SEP IRA?

A Solo 401(k) can be better if you want employee deferrals, Roth options, or catch-up contributions. A SEP IRA may be easier to manage, but it does not offer employee elective deferrals in the same way. For many freelancers, Solo 401(k) Contribution Limits 2026 provide more flexibility.

5. Do I need to file Form 5500-EZ?

You may need to file Form 5500-EZ if your one-participant 401(k) plan has $250,000 or more in assets at the end of the year. The IRS states that one-participant plans generally have this annual filing requirement once they cross that asset level.

Free 2026 Solo 401(k) Contribution Estimator: Ask Your Question Below

Want to know how much you may be able to contribute to a Solo 401(k) in 2026? Use this simple comment-based calculator. Just share a few basic details in the comment section, and I’ll try to help you understand your possible contribution range in simple words.

Please comment with:

- Your age in 2026

- Your business type — freelancer, sole proprietor, LLC, S-Corp, consultant, online business, etc.

- Your estimated 2026 business income

- Do you also have a regular job with a 401(k)? — yes or no

- Do you want Traditional, Roth, or both?

Example comment:

“I am 42 years old, self-employed freelancer, expecting $90,000 income in 2026, no other 401(k), and I want to know whether Traditional or Roth Solo 401(k) is better.”

I’ll reply with a simple explanation of how your Solo 401(k) Contribution Limits 2026 may work based on your situation. This is not personal tax advice, but it can help you understand the basic direction before speaking with a tax professional.

Drop your details below and I’ll help you estimate your 2026 Solo 401(k) contribution range.

Question for readers: Are you planning to use a Solo 401(k), SEP IRA, or Roth IRA in 2026? Comment below — I’ll help you compare which option may fit your situation better.

“Hi, I am Devel Gupta, an entrepreneur and the founder of FinanceWithDevel. With 10 years of experience in teaching and simplifying personal finance, my mission is to help beginners build long-term wealth without the confusing jargon. Whether it’s budgeting, investing, or retirement planning, I believe financial freedom starts with simple, consistent habits. Let’s make money make sense. Connect with me on [ LinkedIn/Twitter ] for more daily tips!”