How Much Emergency Fund Should Americans Save in 2026?

How Much Emergency Fund Should Americans Save in 2026? The simple answer is: most Americans should aim for three to six months of essential expenses, while people with unstable income, dependents, high medical costs, or self-employment income may need six to twelve months. That does not mean every person needs the same dollar amount. A single renter in Ohio, a family of four in California, and a freelancer in New York are not playing the same financial game. Emergency savings are personal because expenses, income stability, debt, health needs, and job security are personal.

The question How Much Emergency Fund Should Americans Save in 2026? matters because many households are still financially stretched. Bankrate’s 2026 emergency savings report found that 85% of Americans say they would need at least three months of expenses saved to feel comfortable, but only 46% actually have that much saved. The Federal Reserve’s latest household data shows that only 63% of adults said they could cover a $400 emergency expense using cash or its equivalent. That means a large share of households are one car repair, medical bill, job cut, or rent shock away from financial stress.

What Is an Emergency Fund?

An emergency fund is money kept aside for real financial shocks, not planned shopping, vacations, upgrades, or lifestyle spending. Think of it as a financial airbag. You hope you never need it, but when something hits suddenly, it protects you from going straight into credit card debt or personal loans. A real emergency can include job loss, urgent medical expenses, necessary home repairs, car repairs, temporary income loss, or sudden travel for family reasons. The Consumer Financial Protection Bureau says the right amount depends on your situation and the kinds of unexpected expenses you have faced before.

The key phrase here is essential expenses. When asking How Much Emergency Fund Should Americans Save in 2026?, you should not calculate your emergency fund based on your full lifestyle. You do not need to save six months of restaurant meals, streaming subscriptions, shopping, vacations, and entertainment. You need to save enough to keep the lights on, rent or mortgage paid, food available, insurance active, transportation running, and basic medical needs covered. That difference matters because it makes the goal less scary and more realistic.

The 2026 Emergency Fund Formula

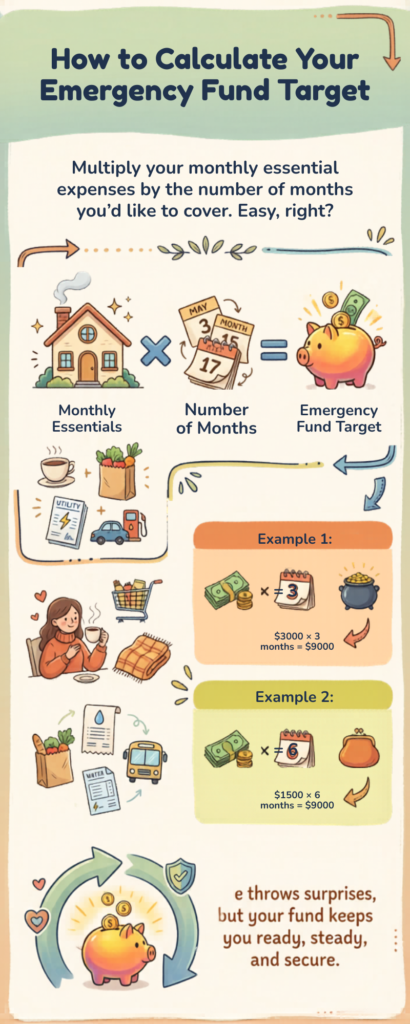

The best formula is simple:

Monthly essential expenses × number of months = emergency fund target

For example, if your essential monthly expenses are $3,000, then a three-month emergency fund is $9,000, a six-month emergency fund is $18,000, and a nine-month emergency fund is $27,000. If your essentials are $5,000 per month, then a six-month fund becomes $30,000. This is why How Much Emergency Fund Should Americans Save in 2026? cannot be answered with one fixed number for everyone.

The latest Bureau of Labor Statistics consumer spending release shows average annual expenditures of $78,535 for U.S. consumer units in 2024, with average income before taxes of $104,207. If you divide the spending figure by 12, that is about $6,544 per month in average total spending. Three months of that is around $19,633, and six months is around $39,268. But remember, total spending is not the same as essential spending. Your real emergency fund should focus on necessary expenses, not every dollar you normally spend.

| Monthly Essential Expenses | 3-Month Fund | 6-Month Fund | 9-Month Fund |

|---|---|---|---|

| $2,000 | $6,000 | $12,000 | $18,000 |

| $3,000 | $9,000 | $18,000 | $27,000 |

| $4,000 | $12,000 | $24,000 | $36,000 |

| $5,000 | $15,000 | $30,000 | $45,000 |

| $6,000 | $18,000 | $36,000 | $54,000 |

How Much Emergency Fund Should Americans Save in 2026 Based on Life Situation?

How Much Emergency Fund Should Americans Save in 2026? For a single person with stable employment, low debt, and no dependents, three to four months of essential expenses may be enough after building a starter fund. This person usually has fewer moving parts. If rent is manageable, healthcare costs are predictable, and income is steady, the emergency fund does not need to be massive from day one. Still, even a single adult should not rely only on credit cards because high-interest debt can turn a small emergency into a long-term financial headache.

For families, How Much Emergency Fund Should Americans Save in 2026? The safer target is usually six months or more. Families have more variables: children, school costs, medical needs, groceries, transportation, rent or mortgage, insurance, and sometimes one income supporting multiple people. If one parent loses a job or a child needs urgent care, expenses do not pause politely. They keep arriving like monthly bills with no emotional intelligence. A family emergency fund should be built around stability, not just survival.

For freelancers, contractors, gig workers, commission-based workers, and small business owners, How Much Emergency Fund Should Americans Save in 2026? A strong target is six to twelve months of essential expenses. Variable income is powerful when things are going well, but it can be brutal when clients delay payments, projects dry up, or business costs rise. Bankrate notes that people who are self-employed may need more than the common three-to-six-month rule because income can be uneven.

For retirees or near-retirees, How Much Emergency Fund Should Americans Save in 2026? The answer depends on Social Security, pension income, healthcare costs, investment withdrawals, and housing status. Retirees may not face job-loss risk in the same way, but they do face medical expenses, market downturns, home repairs, and inflation. A retiree who depends heavily on investments may want a larger cash buffer so they are not forced to sell investments during a bad market. A paid-off home helps, but it does not eliminate emergency costs.

Why Americans Should Not Wait to Build Emergency Savings

Emergency funds are not exciting. Nobody brags at dinner about having six months of rent sitting in a high-yield savings account. But boring money is often the money that saves you. When a car breaks down, your emergency fund becomes transportation. When a job disappears, your emergency fund becomes time. When a medical bill arrives, your emergency fund becomes peace of mind.

The Federal Reserve’s data shows that the share of adults able to cover a $400 emergency with cash or its equivalent stayed at 63% in 2025. That is better than in earlier years, but it still leaves many Americans financially exposed. Bankrate also found a gap between what people feel they need and what they actually have. So, when readers search How Much Emergency Fund Should Americans Save in 2026?, they are not asking a theoretical question. They are asking how to avoid panic when life throws a financial punch.

Where Should You Keep Your Emergency Fund?

Your emergency fund should be safe, liquid, and separate. Safe means you are not investing it in stocks, crypto, or risky assets. Liquid means you can access it quickly when needed. Separate means it should not sit in the same checking account you use for daily spending, because that makes it too easy to slowly drain. CFPB guidance says emergency savings should be accessible, safe, and not too tempting to use for non-emergencies.

A high-yield savings account is usually one of the best places to keep emergency money. It offers access and may pay more interest than a basic checking account. Money market accounts can also work if they are FDIC- or NCUA-insured through a bank or credit union. Some people keep a small amount in checking for immediate emergencies and the rest in high-yield savings. That setup gives you speed and discipline together, which is basically the financial version of keeping snacks nearby but not on your desk.

How to Build an Emergency Fund Faster in 2026

The smartest way to answer How Much Emergency Fund Should Americans Save in 2026? is to break the goal into stages. First, aim for $500 to $1,000. This starter fund can handle small emergencies without forcing you to swipe a credit card. Bankrate quoted Mark Hamrick saying, “Aim for an initial target of $500 in emergency savings,” then automate deposits and keep the money in a high-yield savings account.

After the starter fund, build one month of essential expenses. That is your first serious safety layer. Then move toward three months. Once you hit three months, decide whether your life needs six, nine, or twelve months. If your job is stable and expenses are low, three to six months may be fine. If your income is unpredictable, your family depends on you, or your industry is risky, keep going. The answer to How Much Emergency Fund Should Americans Save in 2026? should always reflect your actual risk, not someone else’s perfect-looking spreadsheet.

Automation is the easiest trick. Set up a recurring transfer after payday, even if it is only $25, $50, or $100. Small savings look weak in the beginning, but they become powerful when repeated. If you save $200 per month, you have $2,400 after one year before interest. Add tax refunds, bonuses, cashback rewards, side income, or unused subscription money, and the fund grows faster. The goal is not to become perfect. The goal is to become harder to financially knock down.

Common Emergency Fund Mistakes to Avoid

The first mistake is saving too little because the full goal feels impossible. If your six-month number is $24,000, you may feel like giving up before starting. Don’t. A $1,000 emergency fund is still better than zero. A one-month fund is better than only $1,000. Personal finance is not a magic switch; it is a staircase. You climb one step at a time.

The second mistake is investing your emergency fund. Your emergency money is not supposed to chase maximum returns. It is supposed to be there when you need it. Stocks can fall. Crypto can crash. Bonds and funds can fluctuate. If your car breaks down during a market dip, you do not want to sell investments at a loss just to pay the mechanic. When asking How Much Emergency Fund Should Americans Save in 2026?, also ask where that money should safely sit.

The third mistake is using emergency savings for non-emergencies. A sale is not an emergency. A new phone is usually not an emergency. A vacation is not an emergency. If you use your safety net for lifestyle spending, you are basically removing the batteries from your smoke alarm because it looks nice on the wall. Keep the fund boring, protected, and clearly labeled.

Conclusion

How Much Emergency Fund Should Americans Save in 2026? Most people should aim for three to six months of essential expenses, but the safest target depends on your income stability, family responsibilities, health needs, debt, and job risk. A stable single worker may be fine with three to four months. A family may need six months or more. A freelancer or business owner may need nine to twelve months. The number is personal, but the purpose is universal: protect your life from becoming financially chaotic when something unexpected happens.

If your target feels too big, start small. Build $500. Then $1,000. Then one month. Then three months. The emergency fund is not about fear; it is about freedom. It gives you breathing room, better decisions, and protection from expensive debt. This article is for educational purposes only and should not be treated as personal financial advice.

FAQs

1. How Much Emergency Fund Should Americans Save in 2026 if they live paycheck to paycheck?

If you live paycheck to paycheck, start with a small emergency fund of $500 to $1,000. After that, aim for one month of essential expenses. You do not need to reach six months immediately. The first goal is to stop small emergencies from turning into credit card debt.

2. How Much Emergency Fund Should Americans Save in 2026 if they are self-employed?

Self-employed Americans should generally aim for six to twelve months of essential expenses. Income can fluctuate, clients may delay payments, and business costs can rise suddenly. A larger fund gives you more time to adjust without panicking.

3. Should emergency savings be based on income or expenses?

Emergency savings should be based on essential expenses, not income. If you earn $8,000 per month but only need $4,000 for essentials, your emergency fund should be calculated from the $4,000 figure. This keeps your goal realistic and practical.

4. Is $10,000 enough for an emergency fund in 2026?

It depends on your monthly expenses. If your essentials are $2,000 per month, then $10,000 covers about five months. If your essentials are $5,000 per month, then $10,000 covers only two months. The right number depends on your real cost of living.

5. Where should Americans keep emergency savings in 2026?

Americans should usually keep emergency savings in a high-yield savings account, money market account, or separate insured savings account. The money should be easy to access, protected from market risk, and separate from daily spending money.

Your Turn: What Would Make You Feel Financially Safe in 2026?

Building an emergency fund is not about copying someone else’s number. It is about finding the amount that lets you sleep better at night. For one person, that might be $5,000. For another family, it might be $25,000 or more. The right number depends on your rent or mortgage, grocery bills, insurance costs, debt payments, job security, and how many people depend on your income.

Now take a minute and think about your own situation. If your income stopped for three months, how much money would you need to stay calm and cover the basics? Would a three-month emergency fund feel enough, or would you feel safer with six months or more?

Try this quick exercise:

| Question | Your Answer |

|---|---|

| What are your monthly essential expenses? | $_____ |

| How many months of safety do you want? | 3 / 6 / 9 / 12 months |

| Your emergency fund target | $_____ |

| How much have you saved so far? | $_____ |

| How much do you still need? | $_____ |

If your number feels too big, don’t panic. Start with your first $500, then build toward $1,000, then one month of expenses. Every dollar saved gives you more breathing room and fewer reasons to rely on credit cards when life gets messy.

What’s your emergency fund goal for 2026? Share your target in the comments — whether it’s $1,000, $10,000, or a full six-month fund. Your answer may help another reader feel less alone and more motivated to start.

Better Comment Question for Engagement

You can also add this line at the end:

Reader question: If you lost your income tomorrow, how many months could your emergency fund cover — less than 1 month, 1–3 months, 3–6 months, or more than 6 months?

This is good because U.S. readers can answer quickly, and quick questions get more comments than long complicated ones.

50/30/20 Budget Rule Explained

A simple budgeting method that can help you divide your income between needs, wants, and savings

“Hi, I am Devel Gupta, an entrepreneur and the founder of FinanceWithDevel. With 10 years of experience in teaching and simplifying personal finance, my mission is to help beginners build long-term wealth without the confusing jargon. Whether it’s budgeting, investing, or retirement planning, I believe financial freedom starts with simple, consistent habits. Let’s make money make sense. Connect with me on [ LinkedIn/Twitter ] for more daily tips!”