mage

Credit card debt can feel frustrating. You make payments every month, but your balance still feels stuck. For many Americans, this is not just a small money problem—it is a real financial stress.

In 2026, credit card debt is still a major issue in the United States. Bankrate reported that 47% of credit cardholders carry debt from month to month, and 61% of credit card debtors have been in debt for at least one year. Bankrate also gave an example showing that a $6,523 credit card balance at 19% APR could take 170 months to pay off if only minimum payments are made.

for more official guidance on credit cards and debts, you can visit the consumer financial protection bureaus credit card her resources.

That is why choosing the right debt payoff method matters.

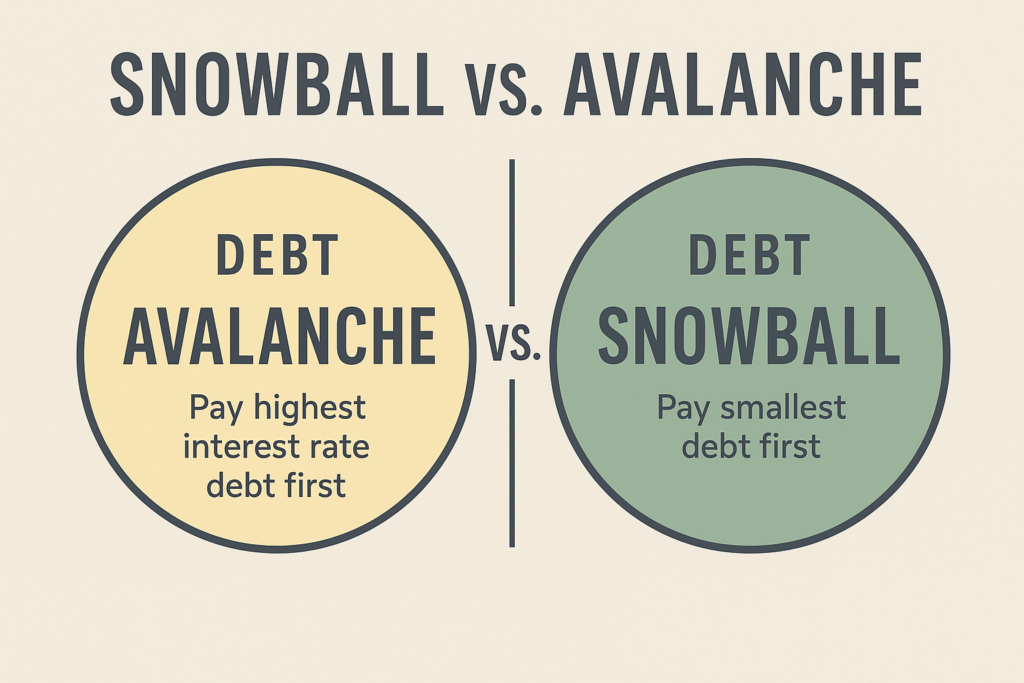

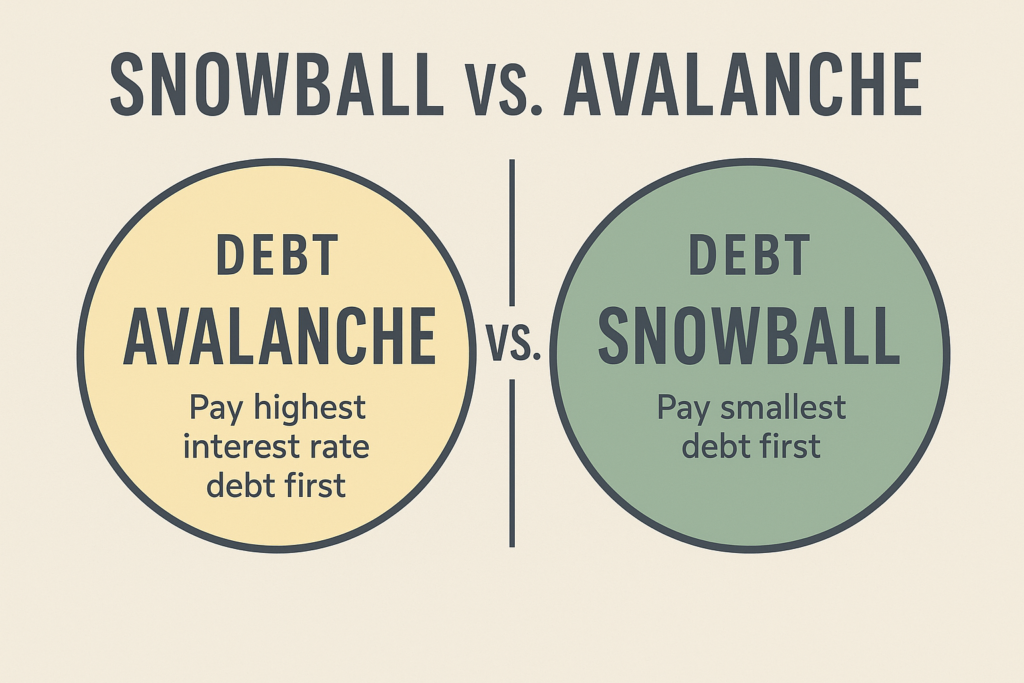

Two of the most popular strategies are the debt snowball method and the debt avalanche method. Both can help you pay off debt, but they work in different ways.

In this guide, you will learn the difference between debt snowball and debt avalanche, which method saves more money, which one is better for beginners, and how to choose the best strategy for your situation.

What Is the Debt Snowball Method?

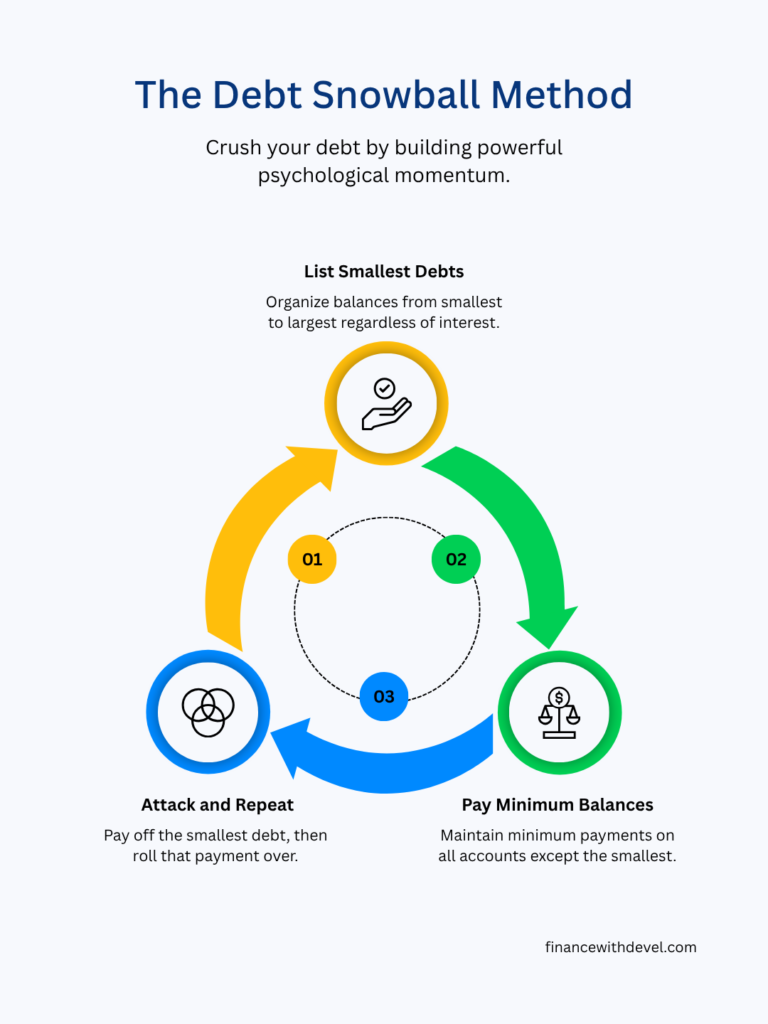

The debt snowball method is a debt payoff strategy where you pay off your smallest debt first.

You make the minimum payment on all your debts, but you put any extra money toward the smallest balance. Once the smallest debt is paid off, you move to the next smallest debt.

when comparing debt snowball vs avalanche , the snowball method is usually better for people who need small wins to stay motivated.

This creates a “snowball” effect. As each debt disappears, you take the money you were paying on that debt and add it to the next one.

Simple Example

Let’s say you have three credit cards:

| Credit Card | Balance | APR |

|---|---|---|

| Card A | $700 | 24% |

| Card B | $2,500 | 29% |

| Card C | $5,000 | 19% |

With the debt snowball method, you would pay off Card A first because it has the smallest balance.

Even though Card B has a higher interest rate, the snowball method focuses on quick wins.

Why the Debt Snowball Method Works

The debt snowball method works because it gives you motivation.

Paying off debt is not only a math problem. It is also an emotional problem. Many people feel tired, ashamed, or overwhelmed when they see multiple balances.

When you pay off one credit card completely, even a small one, you feel progress. That progress gives you confidence to continue.

This is why the snowball method is popular with beginners.

Best For:

The debt snowball method may be best if:

You feel overwhelmed by debt.

You need motivation to keep going.

You have several small balances.

You want to see quick progress.

You have tried debt payoff before but gave up.

The snowball method is not always the cheapest method, but it can be the easiest to stick with.

And in personal finance, the method you actually follow is often better than the method that looks perfect on paper.

What Is the Debt Avalanche Method?

The debt avalanche method is a debt payoff strategy where you pay off the debt with the highest interest rate first.

You still make the minimum payment on every debt. But any extra money goes toward the card or loan with the highest APR.

Once the highest-interest debt is paid off, you move to the next highest interest rate.

in the debt snowball vs avalanche debate, the avalanche method usually saves more money because it targets the highest-interest debt first.

Simple Example

Using the same debts:

| Credit Card | Balance | APR |

|---|---|---|

| Card A | $700 | 24% |

| Card B | $2,500 | 29% |

| Card C | $5,000 | 19% |

With the debt avalanche method, you would pay off Card B first because it has the highest APR.

This method focuses on saving money on interest.

Why the Debt Avalanche Method Works

The debt avalanche method works because it attacks your most expensive debt first.

Credit card interest rates can be high. LendingTree reported that average APRs for credit card accounts accruing interest fell to 21.52% in Q1 2026, but that is still expensive debt.

If you keep a high-interest balance for a long time, you can pay hundreds or thousands of dollars in interest.

The avalanche method reduces that interest cost faster.

This is a key reason why debt snowball vs avalanche matters: avalanche is usually better for saving interest, while snowball is usually better for staying motivated.

Best For:

When choosing debt snowball vs avalanche, the Avalanche Method may be best if:

You want to save the most money.

You are comfortable with numbers.

You can stay motivated without quick wins.

You have one or more very high-interest credit cards.

Your main goal is reducing interest as fast as possible.

The avalanche method is usually the better mathematical choice.

Debt Snowball vs Avalanche: Main Difference

The main difference is simple:

Debt snowball focuses on the smallest balance first.

Debt avalanche focuses on the highest interest rate first.

Debt Snowball vs Avalanche becomes easier to understand when you compare the main goal of each method.

| Feature | Debt Snowball | Debt Avalanche |

|---|---|---|

| First target | Smallest balance | Highest APR |

| Main benefit | Quick motivation | Saves more interest |

| Best for | Beginners and emotional motivation | People focused on math and savings |

| Weakness | May cost more interest | May feel slower at first |

| Style | Psychological strategy | Mathematical strategy |

In short, Debt Snowball vs Avalanche between quick emotional wins and lower interest cost.

Both methods require the same basic habit: pay minimums on all debts and put extra money toward one target debt.

Which Method Saves More Money?

The debt avalanche method usually saves more money.

Why?

Because it pays off the highest-interest debt first. Since high APR debt grows faster, removing it early reduces your total interest cost.

For example, if one credit card has a 29% APR and another has a 17% APR, the 29% card is more expensive. The avalanche method attacks that card first.

That means less interest builds up over time.

So, if your goal is purely financial, avalanche is usually better.

In the debt snowball vs avalanche comparison, avalanche usually wins for saving money because it reduces high interest debt first.

But there is one catch: it may take longer to feel progress.

If your highest-interest card also has a large balance, you may work on it for months before paying it off. Some people lose motivation during that time.

That’s is why debt snowball vs avalanche is not only a math decision ; it is also a motivation decision.

Which Method Is Better for Beginners?

For many beginners, the debt snowball method may be easier.

Not because it saves the most money, but because it builds momentum.

Imagine you have five debts. Paying off one small debt in the first month feels good. It shows you that the plan is working.

That emotional win can be powerful.

If you are new to budgeting, struggling with discipline, or feeling stressed by multiple payments, the snowball method can help you start.

A perfect plan is useless if you quit after two months. A simple plan that keeps you moving is often better.

Example: Paying Off $10,000 in Credit Card Debt

Let’s say you have $10,000 in credit card debt:

| Debt | Balance | APR | Minimum Payment |

|---|---|---|---|

| Card 1 | $1,000 | 22% | $35 |

| Card 2 | $3,000 | 29% | $90 |

| Card 3 | $6,000 | 18% | $180 |

Your total minimum payment is $305.

You create a budget and find an extra $300 per month for debt payoff.

So your total monthly debt payment is:

$305 minimums + $300 extra = $605 per month

With Debt Snowball

You pay minimums on all cards.

Then you put the extra $300 toward Card 1 because it has the smallest balance.

Order:

- Card 1 — $1,000 balance

- Card 2 — $3,000 balance

- Card 3 — $6,000 balance

This gives you a quick win when Card 1 is paid off.

With Debt Avalanche

You pay minimums on all cards.

Then you put the extra $300 toward Card 2 because it has the highest APR.

Order:

- Card 2 — 29% APR

- Card 1 — 22% APR

- Card 3 — 18% APR

This likely saves more money in interest.

Debt Snowball Pros and Cons

Pros of Debt Snowball

1. Quick wins

You can pay off small balances faster. This helps you feel progress early.

2. Simple to understand

You do not need complicated calculations. Just list your debts from smallest to largest.

3. Good for motivation

It is easier to stay consistent when you see debts disappear.

4. Helps reduce mental clutter

Fewer balances mean fewer payments to track.

Cons of Debt Snowball

1. May cost more interest

Because you are not focusing on the highest APR first, you may pay more interest over time.

2. Not the best mathematical strategy

If you have a very high-interest card, ignoring it for too long can be expensive.

3. Can be slower for total savings

You may feel progress emotionally, but financially you may not save as much as avalanche.

Debt Avalanche Pros and Cons

Pros of Debt Avalanche

1. Saves more money

This is usually the biggest advantage. You attack the highest-interest debt first.

2. Reduces expensive debt faster

High APR debt is dangerous. Avalanche removes it early.

3. Best for disciplined people

If you are serious about lowering interest costs, this method is strong.

4. Good for large credit card balances

If most of your debt is high-interest credit card debt, avalanche can be very useful.

Cons of Debt Avalanche

1. Slower emotional progress

If your highest-interest debt has a large balance, it may take longer to pay off your first debt.

2. Harder for beginners

Some people lose motivation if they do not see a balance disappear quickly.

3. Requires more discipline

You need to stay focused even when progress feels slow.

Minimum Payments Are Not Enough

No matter which method you choose, avoid paying only the minimum if possible.

Making the minimum payment helps keep your account in good standing, but paying only the minimum can make debt last much longer and increase interest costs. Bankrate explains that minimum payments can lead to higher interest charges and a longer payoff timeline.

This is why both snowball and avalanche require extra payments.

Even an extra $50, $100, or $200 per month can make a difference.

The basic rule is:

Minimum payments protect your credit. Extra payments create progress.

Should You Use Debt Snowball or Avalanche in 2026?

Here is the simple answer:

The best method is the one you can follow every month without quitting.

Use debt snowball if you need motivation.

Use debt avalanche if you want to save the most money.

But let’s make it even easier.

Choose Debt Snowball If:

You have many small debts.

You feel overwhelmed.

You need quick wins.

You want a simple plan.

You have struggled to stay motivated before.

Choose Debt Avalanche If:

You have high-interest credit card debt.

You want to reduce interest costs.

You are disciplined with your budget.

You can stay focused even if progress feels slow.

You want the mathematically smarter method.

Both methods are better than doing nothing.

A Hybrid Method: The Best of Both

Some people use a hybrid strategy.

Here is how it works:

First, pay off one or two small debts using the snowball method. This gives you quick motivation.

Then switch to the avalanche method and attack the highest-interest debt.

This can be a smart approach because you get both:

Quick emotional wins

Lower interest costs later

Example

If you have one tiny $300 credit card balance, pay it off first. Then attack the card with the highest APR.

This gives your brain a win without ignoring the math for too long.

For many beginners, this hybrid method is the most practical option.

What If You Cannot Pay Extra Right Now?

If you can only make minimum payments right now, do not panic.

Start with small steps.

First, make every minimum payment on time. Then look for ways to free up even a small amount of money.

You can:

Cancel unused subscriptions.

Cook at home a few more times per week.

Pause non-essential shopping.

Sell unused items.

Pick up a small side gig.

Use tax refunds or bonuses for debt.

Call your credit card company and ask about hardship options.

Even if you can add only $25 or $50 per month, that is still progress.

The goal is to build the habit.

Should You Consider Balance Transfers or Debt Consolidation?

A balance transfer or debt consolidation loan can help in some cases, but it is not magic.

A balance transfer moves debt to another credit card, often with a lower promotional APR.

A debt consolidation loan combines multiple debts into one loan, usually with a fixed payment.

These options may help if:

You qualify for a lower rate.

You stop using the old credit cards.

You understand the fees.

You have a real payoff plan.

You do not create new debt again.

They may not help if you transfer debt and continue spending.

Debt payoff tools only work when your habits change too.

How to Start Your Debt Payoff Plan Today

Here is a simple step-by-step plan:

Step 1: List every debt

Write down the balance, APR, minimum payment, and due date.

Step 2: Choose your method

Pick snowball, avalanche, or hybrid.

Step 3: Pay minimums on all debts

This helps avoid late fees and credit damage.

Step 4: Put extra money toward one target debt

Do not spread extra payments across every card. Focus on one target.

Step 5: Track progress every month

Write down your total debt balance monthly.

Step 6: Stop adding new debt

Avoid using credit cards for purchases you cannot pay off.

Step 7: Repeat until debt-free

Once one debt is paid off, move to the next.

Common Mistakes to Avoid

Mistake 1: Choosing a method but not budgeting

Debt payoff needs extra money. Without a budget, the plan is weak.

Mistake 2: Using the credit card while paying it off

This is like trying to empty a bucket while the tap is still running.

Mistake 3: Ignoring APR completely

Interest matters, especially with credit cards.

Mistake 4: Trying to be perfect

You may have bad months. Do not quit. Adjust and continue.

Mistake 5: Not building a small emergency fund

Without emergency savings, one surprise bill can push you back into debt.

Final Verdict: Debt Snowball vs Avalanche

So, which debt payoff method is better?

Debt avalanche is better for saving money.

Debt snowball is better for motivation.

If you are disciplined and want to pay less interest, choose avalanche.

If you feel overwhelmed and need quick wins, choose snowball.

If you want a balanced approach, use the hybrid method: pay off one small debt first, then switch to avalanche.

The best debt payoff method is the one you can follow consistently.

Credit card debt can feel heavy, but it is not permanent. Start with one list, one method, and one extra payment. Small steps can turn into real financial progress.

FAQs

1. Is debt snowball or debt avalanche better?

Debt avalanche is usually better for saving money because it pays off the highest-interest debt first. Debt snowball is better for motivation because it pays off the smallest balance first.

2. Which debt payoff method is best for beginners?

The debt snowball method is often best for beginners because it gives quick wins and keeps motivation high. However, disciplined beginners may prefer the avalanche method to save more interest.

3. Does the debt avalanche method save more money?

Yes, the debt avalanche method usually saves more money because it targets high-interest debt first. This reduces the total interest you pay over time.

4. Does the debt snowball method really work?

Yes, the debt snowball method can work well because it helps people stay motivated. Paying off small debts quickly can create momentum and confidence.

5. Should I pay off the smallest debt or highest interest first?

Pay off the smallest debt first if you need motivation. Pay off the highest-interest debt first if you want to save more money.

6. Can I use both debt snowball and debt avalanche?

Yes. A hybrid method can work well. You can pay off one small debt first for motivation, then switch to the avalanche method to save interest.

7. Should I keep using my credit card while paying off debt?

It is better to avoid adding new credit card debt while paying off old debt. If you keep spending more than you can repay, your progress will slow down.

8. What is the fastest way to pay off credit card debt?

The fastest way is to stop adding new debt, pay more than the minimum, use a clear payoff method, cut unnecessary expenses, and increase income if possible.

“Hi, I am Devel Gupta, an entrepreneur and the founder of FinanceWithDevel. With 10 years of experience in teaching and simplifying personal finance, my mission is to help beginners build long-term wealth without the confusing jargon. Whether it’s budgeting, investing, or retirement planning, I believe financial freedom starts with simple, consistent habits. Let’s make money make sense. Connect with me on [ LinkedIn/Twitter ] for more daily tips!”