In 2026, many Americans are asking the same money question: emergency fund vs credit card debt — should you save cash first or pay off your cards first? With rent, groceries, car insurance, medical bills, and interest rates still putting pressure on household budgets, this decision can feel confusing.

The honest answer is that you usually need both. If you only save money and ignore your card balance, interest can grow fast. But if you put every extra dollar toward debt and keep zero savings, one car repair or medical bill can push you right back into borrowing.

That is why this guide explains the smart middle path. You will learn when to save first, when to attack debt first, and how to build a simple plan that works for real life in the U.S.

Why This Decision Matters in 2026

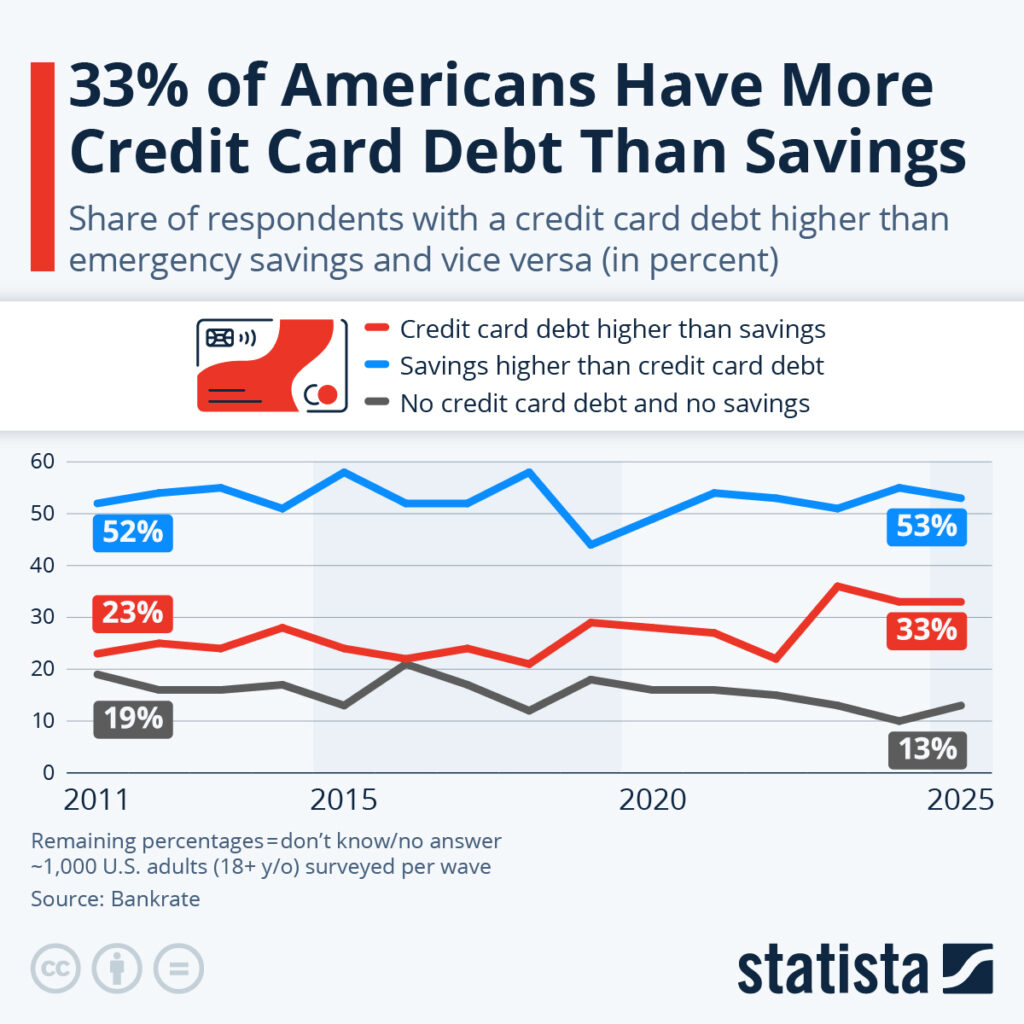

The emergency fund vs credit card debt decision matters because credit cards often charge very high interest. If your card APR is around 20% or more, your balance can become expensive even when you are making minimum payments every month.

At the same time, living without emergency savings is risky. A $600 car repair, a sudden doctor visit, or a temporary job loss can create stress fast. When people do not have savings, they often use credit cards again, and the debt cycle continues.

So the goal is not to be perfect. The goal is to protect yourself from small emergencies while also reducing expensive debt.

What Is an Emergency Fund?

Before comparing emergency fund vs credit card debt, understand what an emergency fund means. It is money kept aside only for unexpected and necessary expenses, not for shopping, vacations, or lifestyle upgrades.

Examples of real emergencies include medical bills, urgent car repairs, job loss, home repairs, or emergency travel. These are situations where having cash can protect you from using a credit card again.

For beginners, a good starter emergency fund is usually $500 to $1,000. It may not cover every problem, but it gives you a basic safety cushion.

What Is Credit Card Debt?

Credit card debt happens when you use your card and do not pay the full balance by the due date. The bank then charges interest on the unpaid amount, and that interest can make your balance grow.

In the emergency fund vs credit card debt debate, credit card debt is dangerous because the interest rate is usually much higher than a normal savings account return. This means keeping a large amount of cash while paying high card interest may not be the best move.

The biggest trap is paying only the minimum amount. Minimum payments may keep your account current, but they can also keep you in debt for years.

Should You Save First or Pay Debt First?

For most people, the best answer to emergency fund vs credit card debt is: save a small starter fund first, then pay high-interest credit card debt aggressively. This gives you protection and progress at the same time.

If you have $0 or very little savings, do not put every extra dollar toward the card immediately. First, build a small cash cushion so a small emergency does not force you to swipe the card again.

Once you have that starter fund, shift most of your extra money toward your highest-interest credit card or your smallest balance, depending on the payoff method you choose.

When You Should Build Savings First

You should focus on savings first if you have no emergency cash at all. Without even a small cushion, almost any unexpected expense can become new debt.

You should also save first if your income is unstable. This includes freelancers, gig workers, commission-based workers, people in seasonal jobs, or anyone worried about layoffs.

This money choice also depends on your family situation. If you have kids, medical expenses, an older car, or a single-income household, having some cash available becomes even more important.

When You Should Pay Credit Card Debt First

You should focus more on debt payoff once you already have a starter emergency fund. After you have $500 to $1,000 saved, high-interest credit card balances should become a top priority.

This is especially true if your APR is above 20%. At that level, the interest cost can be much higher than what you earn in a savings account.

In the emergency fund vs credit card debt plan, paying down cards also helps your monthly cash flow. When balances fall, minimum payments can become easier to manage, and your financial stress may reduce.

Best Strategy: The Balanced 3-Step Plan

The best emergency fund vs credit card debt strategy is a balanced 3-step plan. It is simple, realistic, and easier to follow than extreme advice.

Step 1: Build a starter emergency fund of $500 to $1,000. Keep it in a separate savings account so you do not spend it casually.

Step 2: Pay minimum payments on all cards, then put extra money toward one card at a time. Use debt avalanche if you want to save the most interest, or debt snowball if you need motivation from quick wins.

Step 3: After your high-interest debt is paid down, grow your emergency fund to 3 to 6 months of essential expenses.

Real-Life Example

Let’s say Jessica lives in Ohio and has $6,000 in credit card debt at 24% APR. She has only $150 in savings and can free up $400 per month.

If she puts the full $400 toward debt, the math looks good, but she is still exposed. If her car needs a $700 repair, she may have to use the card again.

A better plan would be to save part of that $400 until she has at least $1,000 in emergency cash. After that, she can send most of the $400 toward the card balance every month.

This way, Jessica is not ignoring debt, but she is also not leaving herself financially helpless.

Debt Avalanche or Debt Snowball?

Once your starter fund is ready, the next question is how to pay the cards. Two popular methods are debt avalanche and debt snowball.

Debt avalanche means you pay the card with the highest interest rate first. This usually saves the most money over time.

Debt snowball means you pay the smallest balance first. This gives faster emotional wins and can help you stay motivated.

For your payoff journey, the best method is the one you will actually follow. If you love numbers, choose avalanche. If you need motivation, choose snowball.

you can also read my guide on debt snowball vs avalanche to compare debt payoff strategies.

How Much Emergency Savings Do You Need?

A starter fund of $500 to $1,000 is a good first target. This is not your final safety net, but it gives you breathing room.

After your high-interest cards are under control, aim for 3 to 6 months of essential expenses. Essential expenses include rent or mortgage, utilities, groceries, insurance, transportation, and basic medical needs.

The right amount depends on your life. A single person with stable income may need less than a family with kids, a mortgage, and one income.

Common Mistakes to Avoid

One common mistake in emergency fund vs credit card debt planning is keeping too much cash while paying very high credit card interest. A big savings balance may feel safe, but expensive interest can quietly damage your finances.

Another mistake is using all your cash to pay debt and keeping nothing for emergencies. That can lead to a cycle where you pay the card, face a surprise bill, and use the card again.

A third mistake is continuing the same spending habits while trying to pay off debt. If the card is still being used for lifestyle spending, the payoff plan will not work.

Simple Monthly Action Plan

Start by listing your income, rent or mortgage, utilities, groceries, gas, insurance, minimum card payments, and subscriptions. This shows you where your money is going.

Next, cut or reduce non-essential spending for 60 to 90 days. Food delivery, unused subscriptions, impulse shopping, and expensive entertainment are good places to look first.

Then use the extra cash to build your starter fund. After that, send the extra money to your credit cards every month.

The emergency fund vs credit card debt plan works best when you stop adding new balances. Try to use your card only when you can pay it in full.

Final Answer

The final answer is simple: build a small emergency fund first, then attack high-interest credit card debt. After the expensive debt is under control, build a bigger safety net.

If you have no savings, your first target should be $500 to $1,000. If you already have that amount, your next target should be your credit card balance.

In 2026, emergency fund vs credit card debt is not about choosing one forever. It is about choosing the right order so you can avoid new debt and slowly become financially stronger.

Conclusion

Money decisions feel stressful when every bill is fighting for attention. But with a simple plan, you can make progress without feeling lost.

Start small, stay consistent, and avoid new debt as much as possible. A little savings plus regular debt payoff can change your financial life over time.

The best emergency fund vs credit card debt approach is the one that protects you today and moves you closer to debt freedom tomorrow.

FAQs

1. Should I save money or pay off credit card debt first?

You should usually save a small starter fund first, then pay off high-interest credit card debt aggressively.

2. Is $1,000 enough for an emergency fund?

$1,000 is a good starter amount, but a full emergency fund is usually 3 to 6 months of essential expenses.

3. Should I use my full emergency fund to pay off credit card debt?

No, do not empty your entire emergency fund. Keep at least a small cushion for unexpected expenses.

4. Which payoff method is better after building savings?

Debt avalanche saves more interest, while debt snowball gives faster motivation. Choose the one you can follow consistently.

5. What is the best plan for 2026?

The best plan is to build a starter emergency fund, stop adding new card balances, and then pay down high-interest debt every month.

For official consumer finance guidance, you can also visit the Consumer Financial Protection Bureau credit card resources.

” If you decide to clear your debt first, you can use the [ Debt snowball vs Avalanche] method”

“Hi, I am Devel Gupta, an entrepreneur and the founder of FinanceWithDevel. With 10 years of experience in teaching and simplifying personal finance, my mission is to help beginners build long-term wealth without the confusing jargon. Whether it’s budgeting, investing, or retirement planning, I believe financial freedom starts with simple, consistent habits. Let’s make money make sense. Connect with me on [ LinkedIn/Twitter ] for more daily tips!”