Credit utilization is the percentage of your available revolving credit that you are currently using. In simple words, it tells lenders how much of your credit card limit you have already spent. Experian defines credit utilization as the amount of revolving credit you are using divided by your total revolving credit available, and it says this number can be an important factor in your credit scores. Think of it like this: your credit limit is the size of your water tank, and your balance is how much water you have already used. If your tank is almost empty, lenders may feel you are managing your credit comfortably. But if your tank is nearly full, it may look like you are depending too much on borrowed money.

This matters because credit cards are not just payment tools; they are also signals. Every month, your card issuer usually reports your balance and credit limit to the credit bureaus. That reported information can affect how credit scoring models view your risk. A person who uses a small part of their limit and pays on time looks different from someone who keeps multiple cards close to maxed out. The first person looks controlled, while the second person may look financially stretched, even if both people earn the same income.

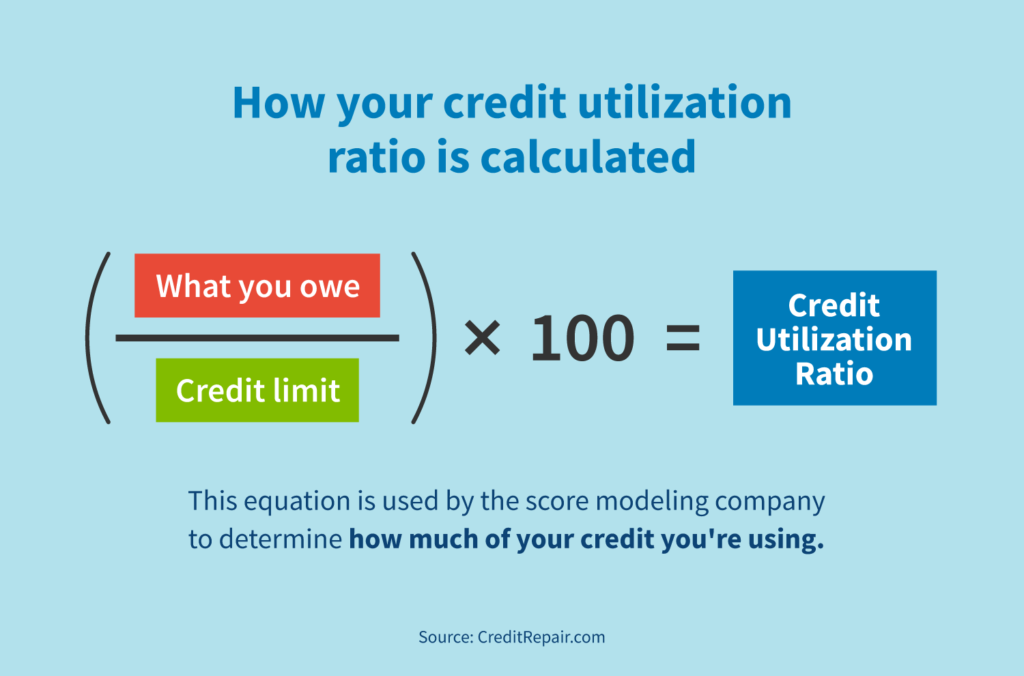

The Simple Formula

The credit utilization formula is easy: divide your credit card balance by your credit limit, then multiply by 100. If your credit card balance is $500 and your credit limit is $2,000, your utilization is 25%. The math looks like this: $500 ÷ $2,000 × 100 = 25%. That means you are using one-fourth of your available credit. Nothing complicated, no finance degree needed, no scary bank language.

Where people get confused is that the balance used for scoring is often the balance reported to the credit bureaus, not necessarily the balance you see after paying your bill later. Experian notes that utilization is based on the balances that appear in your credit report, which may be different from your real-time card balance. So, you could pay your card in full by the due date and still show high utilization if the statement closed when your balance was high. This is why timing matters. Paying before your statement closes can sometimes help reduce the balance that gets reported.

Overall Utilization vs. Per-Card Utilization

There are two types of credit utilization you should understand: overall utilization and per-card utilization. Overall utilization looks at all your revolving balances compared with all your revolving limits. Per-card utilization looks at each credit card separately. For example, if you have three cards with a total limit of $10,000 and total balances of $2,000, your overall utilization is 20%. That sounds good, right?

But here is the sneaky part. If one card has a $1,000 limit and a $950 balance, that single card is at 95% utilization. Experian says scoring models may consider both overall utilization and the highest utilization rate on an individual revolving account. So even if your total utilization looks okay, maxing out one card can still hurt. It is like saying your whole house is clean while one room has clothes, plates, and Amazon boxes everywhere. The overall picture matters, but the messy room still counts.

Why Credit Utilization Matters for Your Credit Score

Credit utilization matters because it helps credit scoring models judge how dependent you are on revolving debt.

FICO says the “amounts owed” category makes up 30% of a FICO Score, and using a high percentage of available credit may indicate that a borrower is overextended. That does not mean having credit card debt automatically makes you a bad borrower. It simply means that the higher your balances are compared with your limits, the more risk you may appear to carry.

This is especially important in the U.S. because credit scores influence so many real-life decisions. A stronger score can help when applying for credit cards, auto loans, mortgages, rental housing, and sometimes even utility accounts. Credit card debt is also a major part of the American money picture.

The New York Fed reported that total U.S. household debt reached about $18.8 trillion in the first quarter of 2026, while credit card balances stood around $1.25 trillion after falling by $25 billion during the quarter. That means millions of people are juggling credit cards, and small habits around utilization can have a meaningful effect.

How FICO Looks at Revolving Debt

FICO does not look only at the dollar amount you owe. It also looks at how that amount compares with your credit limits. FICO explains credit utilization as the percentage of amounts owed compared with the credit limit, and says that “typically, the lower your credit utilization the better.” So, owing $1,000 is not automatically good or bad. If your limit is $1,200, that is a high-risk-looking 83% utilization. If your limit is $20,000, that same $1,000 balance is only 5%.

This is why two people can owe the same amount but have very different credit-score outcomes. Person A owes $2,000 on a $2,500 limit. Person B owes $2,000 on a $20,000 limit. Person A looks close to maxed out, while Person B looks like they are using credit lightly. The debt amount is the same, but the context is completely different. Credit scoring is often about context, not just raw numbers.

Why Lenders Care About Your Available Credit

Lenders care about credit utilization because it can signal financial pressure. If you are regularly using most of your credit limit, a lender may wonder whether you are relying on debt to manage everyday expenses. That may not be true in your case—you might simply be earning rewards and paying in full—but the score only sees reported balances, not your full life story. The credit report does not know that you bought groceries, gas, flights, or business expenses and planned to pay everything next week.

The CFPB’s 2025 credit card market report reviewed the U.S. credit card market as of the end of 2024 and noted that credit card debt exceeded $1.2 trillion, with purchase volume growing to $3.6 trillion in 2024. That shows how deeply credit cards are woven into American spending. When balances are high, lenders may see more risk. When balances are low relative to limits, lenders may see more breathing room. In simple terms, available credit is like oxygen in your financial system—the less oxygen left, the more uncomfortable things look.

What Is a Good Credit Utilization Ratio?

A good credit utilization ratio is generally low, but there is no single magic number that works perfectly for everyone. You have probably heard the famous rule: keep utilization below 30%. That is useful as a beginner guideline, but it is not a hard credit-score border. my FICO says some experts recommend staying below 30%, but the data does not support the idea that your score suddenly dips the moment you cross 30%. Credit scores are not like a video game where you step on one tile and instantly lose points. They are more like a dimmer switch: as utilization rises, risk can rise gradually.

For many people, staying below 30% is a reasonable starting target. But if you want to optimize your score before applying for a mortgage, auto loan, or premium credit card, lower is usually better. Experian says people in the highest credit score range tend to have utilization rates in the single digits. That does not mean you need to become obsessive and panic over every purchase. It means if you can keep your reported balances low, your score may thank you.

The 30% Rule Explained

The 30% rule means you try not to let your reported balance exceed 30% of your credit limit. If your card limit is $1,000, 30% is $300. If your total credit limit across all cards is $10,000, 30% is $3,000. This rule is popular because it is easy to remember and helps people avoid looking overextended. It is not perfect, but it is useful for everyday cardholders who want a simple guardrail.

Here is the important part: 30% should not be your goal; it should be more like your warning light. If your utilization is often around 28% or 29%, you are technically under the rule, but you may still be higher than ideal for score optimization. A better practical target is often under 10% when you are preparing for a major loan application. But for normal months, especially when life gets expensive, staying under 30% is still much better than running cards close to the limit.

Why Single-Digit Utilization Can Be Better

Single-digit credit utilization means your reported balance is below 10% of your available credit. For example, if your total credit limit is $10,000, a reported balance under $1,000 would be single-digit utilization. myFICO says generally keeping utilization below 10%, while consistently paying bills on time, can help build and maintain a good FICO Score. That is why many credit enthusiasts aim for 1% to 9% utilization when they want their score to look its best.

But here is a small twist: 0% utilization is not always ideal. Experian says 0% utilization can be worse than 1% because scoring models need some usage to evaluate credit habits. So, if you want to be extra strategic, you might let one small balance report, then pay it off by the due date. This shows activity without showing dependence. It is like showing up to the gym just enough that the trainer knows you exist, but not so much that you collapse on the treadmill.

| Utilization Range | What It Usually Signals | Smart Action |

|---|---|---|

| 0% | No reported revolving use | Use lightly if you want activity reported |

| 1%–9% | Very low usage | Often ideal before big credit applications |

| 10%–29% | Moderate, usually manageable | Good everyday target for many users |

| 30%–49% | Higher usage | Start paying down before it becomes stressful |

| 50%+ | Heavy dependence on credit | Prioritize reducing balances quickly |

| 90%–100% | Near maxed out | High risk signal; avoid if possible |

Credit Utilization Examples You Can Actually Understand

Let’s make credit utilization feel real, because this topic becomes much easier when you see numbers. Imagine your credit card is like a parking lot. Your credit limit is the total number of parking spaces, and your balance is the number of spaces already filled. If only a few spaces are taken, the parking lot looks relaxed. If almost every space is full, anyone driving by can tell it is crowded. Credit utilization works the same way: the more of your limit you use, the more crowded your credit profile can look.

The nice thing is that utilization is one of the more flexible credit-score factors. A missed payment can stay on a credit report for years, but many scoring models focus heavily on your most recently reported utilization. Experian says many credit scores only consider current utilization based on recently reported balances and limits, which means lowering utilization can sometimes help scores recover quickly. That is good news. It means you are not stuck forever just because you had one expensive month.

Example With One Card

Suppose you have one credit card with a $5,000 credit limit. If your balance is $500, your utilization is 10%. If your balance is $1,500, your utilization is 30%. If your balance is $4,500, your utilization is 90%. Same card, same person, same limit—but three very different signals.

Now imagine you pay the $4,500 balance down to $400 before the card issuer reports to the credit bureaus. Your utilization drops from 90% to 8%. That change may make your profile look much healthier. The key is not just paying eventually; the key is understanding when the balance gets reported. Paying by the due date protects you from interest and late fees, but paying before the statement closing date can help reduce reported utilization.

Example With Multiple Cards

Now let’s say you have three cards. Card A has a $3,000 limit and a $300 balance. Card B has a $5,000 limit and a $500 balance. Card C has a $2,000 limit and a $1,800 balance. Your total limit is $10,000, and your total balance is $2,600, so your overall utilization is 26%. That sounds okay because it is under 30%.

But Card C is at 90% utilization by itself. That individual card may still be a problem because it looks nearly maxed out. A smarter move could be paying down Card C first, even if your overall utilization is not terrible. You could also spread spending more evenly in future months, but be careful not to use that as an excuse to spend more. The goal is not to play musical chairs with debt. The goal is to keep balances low and manageable.

Smart Ways to Lower Your Credit Utilization

Lowering credit utilization is mainly about two levers: reduce balances or increase limits. Reducing balances is usually safer because it also lowers debt. Increasing limits can help mathematically, but only if you do not use the extra limit as permission to spend more. If your credit limit rises from $5,000 to $10,000 and your balance stays $1,000, your utilization drops from 20% to 10%. But if you celebrate the higher limit by spending another $3,000, the benefit disappears.

This is where smart credit card use becomes less about tricks and more about habits. The best system is boring in the best possible way: spend what you can afford, pay on time, keep reported balances low, and avoid treating credit cards like extra income. Credit cards can give rewards, fraud protection, and convenience, but they can also become expensive if balances roll over with interest. The card is a tool. A hammer can build a house or smash a window. Same tool, different behavior.

Pay Before the Statement Closes

One of the most practical ways to lower credit utilization is to pay before your statement closing date. Many card issuers report your balance around the end of the statement period, not after your due date. Experian explains that issuers generally report balances at the end of each statement period, and making a payment before that date may lower the reported balance. This is a big deal because many people pay in full and still show high utilization simply because the timing is off.

Here is a simple routine: check your card balance a few days before the statement closes, pay it down to a low amount, let a small balance report if you want activity, then pay the rest by the due date. This does not mean you need to micromanage every cup of coffee. But before applying for a major loan, this habit can help your score look cleaner. Think of it like dressing well for an interview. You may be the same person underneath, but presentation matters.

Request a Higher Credit Limit Carefully

Another way to lower credit utilization is to request a higher credit limit. If your income has increased, your payment history is strong, and you are not tempted to overspend, a higher limit can improve your utilization ratio. Experian notes that requesting a higher credit limit may help, especially after your income rises, your credit score improves, or you pay off other debts, though some requests can trigger a hard inquiry. So yes, this can work, but do not do it blindly.

The danger is psychological. A higher limit can feel like extra money, but it is not income. It is just a bigger borrowing ceiling. If you are already struggling with overspending, asking for more credit might make the problem worse. Use this strategy only if you have discipline. The best credit limit increase is the one you barely use.

Keep Old Credit Cards Open

Keeping old credit cards open can help your credit utilization because those unused limits still count toward your available credit. myFICO says closing a credit card removes available credit and could increase overall utilization. For example, if you have $10,000 in total limits and $1,000 in balances, your utilization is 10%. If you close a card with a $5,000 limit, your available credit falls to $5,000, and the same $1,000 balance becomes 20%.

That does not mean you should keep every card forever. If a card has a high annual fee and you do not use the benefits, closing it or downgrading it may make sense. If a card tempts you to overspend, closing it may protect your finances even if utilization changes. Credit score optimization should never come before real financial health. A slightly lower score is better than a life full of expensive debt.

Spread Spending Across Cards

Spreading spending across cards can help avoid maxing out one card, but this strategy should be used carefully. If you put $1,500 on one card with a $2,000 limit, that card hits 75% utilization. If you split the same $1,500 across three cards with larger combined limits, your per-card utilization may look better. This can be useful during travel, holidays, home repairs, or other high-spending months.

But spreading spending is not the same as reducing debt. If the total amount is still too high, your overall utilization can still hurt you. The cleanest strategy is to spend less, pay earlier, or use cash/debit for purchases you cannot pay off quickly. Credit cards should make life smoother, not heavier. If spreading balances feels like hiding clutter in different rooms, it is time to clean the house.

Common Credit Utilization Mistakes

Many people misunderstand credit utilization because credit advice online can be oversimplified. One person says never go above 30%. Another says keep 1% exactly. Someone else says carry a balance to build credit, which is one of the most expensive myths out there. The truth is simpler: use credit lightly, pay on time, avoid interest, and keep your reported balances low. That is the foundation.

The bigger mistake is thinking credit score management is the same as money management. A good score is useful, but it is not the final goal. The final goal is financial flexibility. If you have a 780 score but carry high-interest debt every month, you are still bleeding money. If you have a slightly lower score but no credit card debt and healthy savings, you may be in a much stronger real-life position.

Thinking 30% Is a Magic Line

The 30% rule is helpful, but it is not magic. myFICO clearly says the data does not support the idea that your score automatically drops once utilization crosses 30%. That means you should not panic if you hit 31% once, especially if you pay it down quickly. Life happens. Cars break, medical bills appear, flights get expensive, and sometimes the grocery bill looks like it went to private school.

At the same time, do not use that as permission to sit at 60% or 80% utilization for months. Higher utilization can still weigh on your score and may signal financial stress. Treat 30% like a speed-limit sign in a tricky neighborhood. Going slightly over once is not the end of the world, but constantly speeding is asking for trouble.

Closing Cards Too Quickly

Closing a card can accidentally increase your credit utilization by reducing your total available credit. Experian also says closing a card can increase utilization because it decreases overall available credit. This is why people sometimes see a score dip after closing a card, even though they thought they were being responsible. They did reduce complexity, but they also removed part of their credit limit.

Before closing a card, look at the whole picture. Does it have an annual fee? Do you use it? Does it tempt you to overspend? Can you downgrade it to a no-fee version instead? There is no one-size-fits-all answer. A card that is harmless and fee-free may be worth keeping open. A card that causes bad habits may need to go.

Carrying a Balance for Your Score

One of the worst credit myths is that you need to carry a balance and pay interest to build credit. You do not. You can use a credit card, let a small balance report if needed, and then pay the full statement balance by the due date. That shows activity without donating money to the bank in interest. Carrying a balance month to month is not a smart score strategy; it is usually just expensive.

Remember, credit card interest can turn small purchases into long-term pain. If you buy $700 worth of things and only make minimum payments, the balance can linger like an unwanted guest. A good credit score should help you save money, not cost you money. The smartest credit card users enjoy rewards and convenience while avoiding interest as much as possible.

Credit Utilization and Real-Life Money Decisions

Credit utilization becomes especially important before big financial moves. If you are applying for a mortgage, auto loan, apartment, student loan refinance, or a new premium credit card, your score may matter more than usual. In those moments, lowering reported utilization can be one of the faster ways to polish your credit profile. It is not a miracle button, but it can help if high utilization is dragging your score down.

The CFPB says its Consumer Credit Trends dashboards track credit cards and other markets monthly to monitor consumer credit conditions. That matters because credit conditions change, lenders adjust standards, and borrowers with stronger profiles usually have more options. When lenders become stricter, small details can matter more. A clean utilization ratio may not guarantee approval, but it can make your application look healthier.

Before Applying for a Mortgage, Auto Loan, or New Card

Before applying for major credit, try to lower your reported credit utilization for at least one or two statement cycles. Pay down balances, avoid large purchases, and check when each card reports. If you can get utilization into the single digits without creating cash-flow stress, that may help your score look stronger. Also avoid opening several new accounts right before a mortgage application unless you have a specific reason.

This is not about pretending to be richer than you are. It is about making sure the credit report shows your best normal behavior. If you pay in full every month but your report always catches you at a high balance, lenders may not see the full story. Paying before statement close can help your report reflect how you actually manage money. Small timing changes can make your credit profile look much cleaner.

During High-Spending Months

High-spending months are where credit utilization can sneak up on you. Holidays, back-to-school shopping, weddings, medical bills, travel, and home repairs can push balances higher than usual. If you know a big month is coming, plan ahead. You can make multiple payments during the month, use savings for planned expenses, or split purchases carefully without increasing total debt.

The goal is not to fear credit cards. The goal is to control them. A credit card should be like a sharp kitchen knife: useful, powerful, and safe when handled properly. But if you swing it around carelessly, it can hurt you. Use your card for convenience and protection, but let your budget—not your credit limit—decide how much you spend.

Conclusion

Credit utilization is one of the simplest credit concepts to understand and one of the most powerful to manage. It shows how much of your available revolving credit you are using, and it can affect your credit score because lenders see high utilization as a possible sign of financial pressure. The basic formula is balance divided by credit limit, but the real strategy is knowing when balances are reported and keeping them low before that happens. The 30% rule is a helpful beginner guideline, but lower is usually better, especially if you are preparing for a major credit application.

The smartest way to use credit cards is not to avoid them completely or max them out for rewards. It is to use them like tools: spend only what you can repay, pay on time, keep utilization low, and avoid unnecessary interest. If you can stay under 30% for normal use and aim for single digits before important applications, you are already ahead of many cardholders. Credit cards can either work for you or quietly work against you. The difference is not the card—it is the system you build around it.

FAQs

1. What is credit utilization in simple terms?

Credit utilization is the percentage of your credit card limit that you are currently using. If your credit limit is $1,000 and your balance is $250, your utilization is 25%. It helps lenders understand how heavily you rely on credit. Lower utilization usually looks better because it suggests you are not overextended.

2. Is 30% credit utilization good?

Keeping credit utilization under 30% is a useful guideline, but it is not a magic rule. Your score does not automatically crash at 31%. Still, lower is generally better. For stronger score optimization, especially before applying for a loan, many people aim for under 10%.

3. Does 0% utilization help my credit score?

Not always. A 0% utilization rate means no balance is being reported, which may give scoring models less information about your credit use. Very low utilization, such as 1% to 9%, can sometimes be better than 0%. The key is to pay the balance in full by the due date so you avoid interest.

4. How can I lower my credit utilization quickly?

You can lower credit utilization quickly by paying down balances before the statement closing date, making multiple payments during the month, requesting a higher credit limit, or keeping old no-fee cards open. The fastest method is usually paying down the balance before it gets reported to the credit bureaus.

5. Should I carry a balance to improve my credit score?

No, you do not need to carry a balance and pay interest to build credit. You can use your card, let a small balance report if you want activity, and then pay the full statement balance by the due date. Carrying debt month to month usually costs money and is not necessary for a good score.

Managing credit utilization is only one part of good money management. If you are dealing with debt, read our [ Emergency Fund vs Credit Card Debt ] guide to choose a smarter payoff strategy.

“Hi, I am Devel Gupta, an entrepreneur and the founder of FinanceWithDevel. With 10 years of experience in teaching and simplifying personal finance, my mission is to help beginners build long-term wealth without the confusing jargon. Whether it’s budgeting, investing, or retirement planning, I believe financial freedom starts with simple, consistent habits. Let’s make money make sense. Connect with me on [ LinkedIn/Twitter ] for more daily tips!”