Introduction

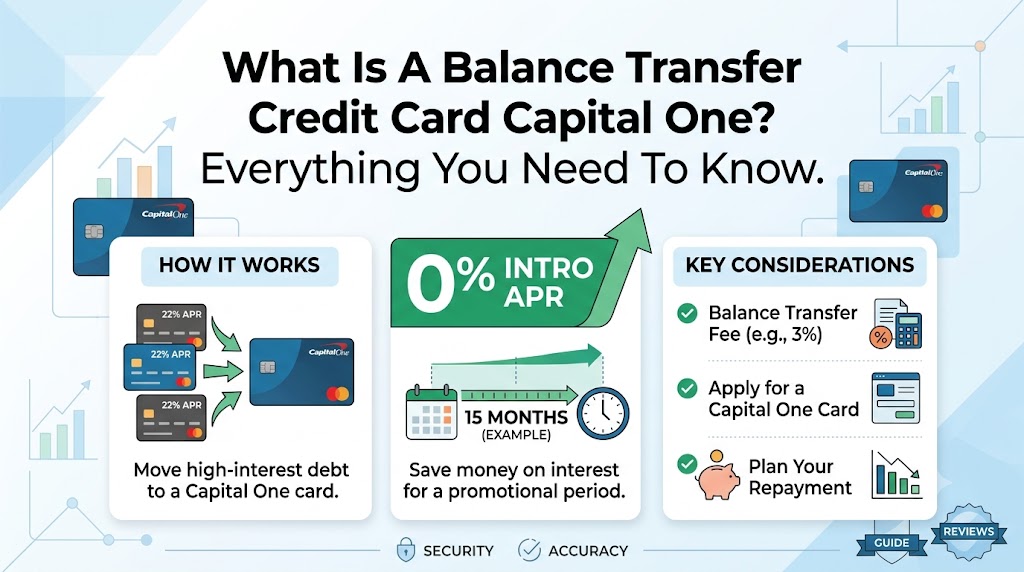

If a high credit card APR is slowing down your debt payoff progress, you might be asking yourself: What is a balance transfer credit card Capital One offering right now to help me save money? The simple answer is that moving your debt to a Capital One balance transfer card can give you some much-needed breathing room. Capital One allows you to transfer various types of unpaid debt—including high-interest credit card balances, personal loans, student loans, and auto loans—to a new card with a lower promotional rate.

The Bottom Line

If you need a balance transfer credit card, Capital One offers several competitive rewards cards featuring 0% introductory APR periods on balance transfers, making them strong tools for debt consolidation. However, you cannot transfer balances between two Capital One accounts, and promotional terms can vary significantly based on the specific offer you receive. Always review your exact pricing terms before applying.

How does a balance transfer credit card Capital One work?

A balance transfer card allows you to shift existing high-interest debt from one financial institution to another. Capital One makes the transfer request process straightforward, allowing you to initiate it online or over the phone. You will need to provide your old account details, the financial institution’s name, and the exact amount you wish to transfer.

Before applying, keep these key rules in mind:

- No Internal Transfers: You cannot transfer debt between two cards issued by Capital One or its affiliates.

- Credit Limit Restrictions: Your total transfer amount plus the associated balance transfer fee cannot exceed your approved credit limit.

- Processing Timeline: Transfers generally post within 4 to 6 days, but they can take up to 15 business days if Capital One needs to issue a physical check to your old lender.

- Keep Paying the Old Card: Continue making minimum payments on your old account until you officially confirm that the balance transfer has cleared.

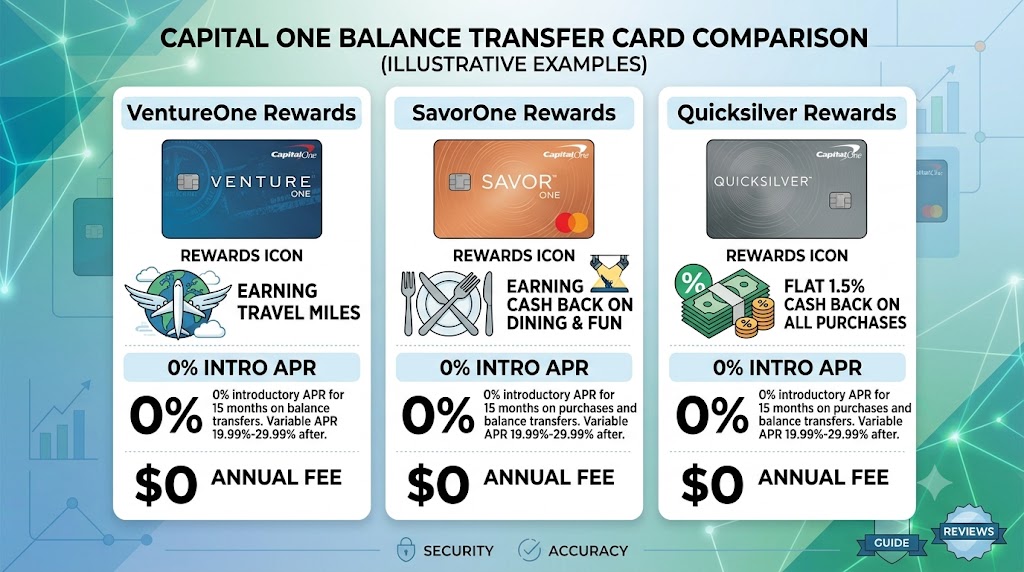

Capital One Balance Transfer Cards Compared

Choosing a balance transfer credit card Capital One provides depends heavily on your credit score and payoff timeline.

| Card Option | Balance Transfer Fee | Intro APR Period | Regular Variable APR | Credit Score Needed | Best Use Case |

|---|---|---|---|---|---|

| Capital One Quicksilver Cash Rewards | 3% fee in the first 15 months (4% on later promotional transfers) | 0% intro APR for 15 months on purchases and balance transfers | 18.49% – 28.49% | Good to Excellent | Straightforward cash back with a longer payoff window |

| Capital One Savor Cash Rewards | Fee applies (verify exact pricing terms) | 0% intro APR for 12 months on purchases and balance transfers | 18.49% – 28.49% | Good to Excellent | Maximizing rewards on dining, groceries, and entertainment |

| Capital One VentureOne Rewards | Varies by offer (up to 4% fee on promotional transfers) | Low intro APR for 15 months (terms vary by channel offer) | 18.49% – 28.49% | Good to Excellent | Earning travel rewards while managing debt |

Pros and Cons

Pros

- Substantial Interest Savings: Eliminating interest charges during the introductory window helps you pay off debt faster.

- Streamlined Finances: Consolidating multiple balances into a single monthly payment simplifies your budget.

- Ongoing Rewards: You can earn cash back or travel miles on new purchases once your transferred balance is paid off.

- Credit Score Improvement: Lowering your credit utilization ratio and maintaining on-time payments can boost your credit health over time.

Cons

- Upfront Fees: Upfront transfer fees reduce your net savings.

- High Regular APR: If you carry a balance past the promotional window, the regular variable APR can be high.

- Hard Credit Inquiry: Applying triggers a hard credit pull, which may temporarily dip your credit score.

- Product Version Risks: Some applicants may be approved for a secondary card version that does not include the promotional 0% APR offer.

- Hard Credit Inquiry: Applying triggers a hard credit pull, which may temporarily lower your credit score. If you want to keep track of your credit health and monitor for any inaccuracies, you can regularly check your reports for free at AnnualCreditReport.com.

How Much Can You Save?

To see if getting a balance transfer credit card Capital One provides makes sense, you must weigh the upfront transfer fee

- Scenario 1: You owe $5,000 on a card with a 24% APR and plan to pay it off over 12 months. Keeping the debt there will cost you roughly $670 in interest. Moving it to a 0% intro APR card with a 3% fee costs $150 upfront. Your estimated savings: $520.

- Scenario 2: You owe $8,000 at a 22% APR and utilize a 15-month introductory window. Leaving it on the old card costs around $1,150 in interest. A 3% balance transfer fee costs $240. Your estimated savings: $910.

Who Should Consider (and Avoid) These Cards?

Consider applying for a balance transfer credit card Capital One offers if you:

- Have good-to-excellent credit (typically a score of 670 or higher).

- Can consistently afford to pay more than the minimum monthly requirement.

- Hold high-interest debt outside of Capital One’s ecosystem.

- Have a clear timeline to wipe out the balance before the promotional window closes.

Avoid these cards if you:

- Are trying to consolidate debt from an existing Capital One account.

- Have an unpredictable monthly income that makes steady payments difficult.

- Plan to continue accumulating new retail debt while paying off the transfer.

- Are at risk of missing monthly deadlines, which can void your promotional rate.

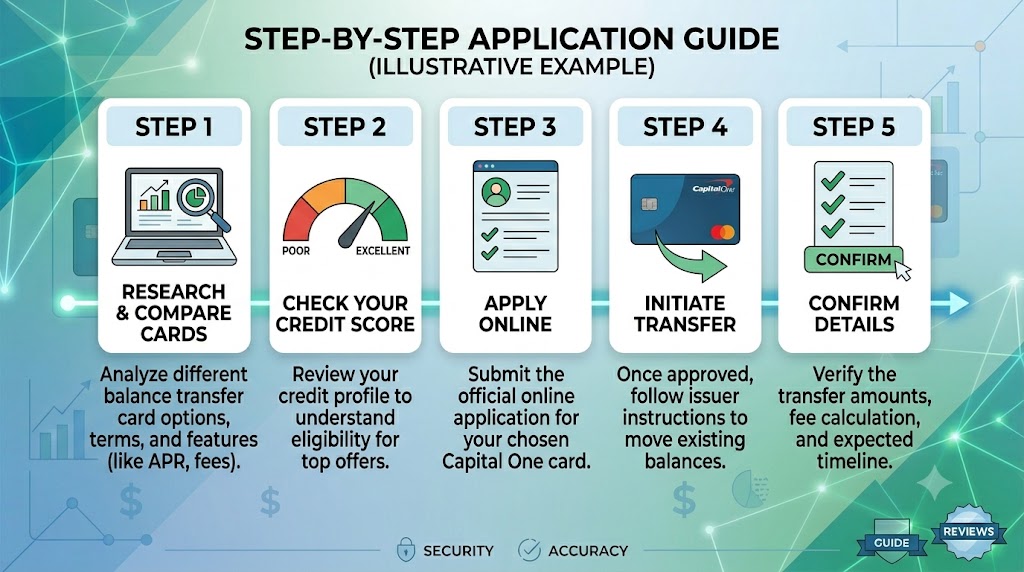

How to Maximize Your Balance Transfer

Once you are approved for a balance transfer credit card Capital One issues, to utilise a promotional APR period successfully, treat the end of the introductory window as a strict deadline.

- Calculate Total Debt: Total up the exact debt balances you intend to move.

- Review Current Interest: Audit your current monthly interest statements to establish a baseline.

- Compare Fine Print: Contrast upfront transfer fees against the length of the promotional period.

- Create a Payment Plan: Divide your total transferred balance (including the fee) by the number of promotional months to determine your ideal fixed monthly payment.

- Automate Your Budget: Set up automatic monthly payments for that specific amount.

- Freeze Extra Spending: Avoid making new purchases on the card until the transferred balance reaches zero.

How We Rate Balance Transfer Cards

At [FinanceWithDevel.com], our primary goal is to provide you with unbiased, accurate, and actionable financial information. To compare and rank these Capital One balance transfer credit cards, our editorial team closely evaluated the following key factors:

- Length of Promotional APR: We gave the highest weight to how many months the card offers a 0% introductory APR (such as 12 or 15 months). The longer the period, the more time you have to comfortably clear your debt.

- Upfront Balance Transfer Fees: We factored in the hidden costs and transfer fees (typically 3% to 4%). A truly valuable balance transfer card is one where the fee is significantly lower than your projected interest savings.

- Long-Term Value (Rewards & Perks): Paying off debt isn’t the only important factor; we also looked at what value the card provides once the balance is zero. Cards like the Quicksilver and Savor were evaluated based on their ongoing cash back and travel rewards.

- Regular Variable APR: The standard interest rates (18.49% – 28.49%) that kick in after the promotional window expires were also taken into account so you understand the true long-term costs.

Editorial Note: This review is entirely independent. Our recommendations are based solely on data, interest terms, and potential user savings, and are not influenced by any credit card issuer.

Frequently Asked Questions

Is the balance transfer credit card Capital One offers good for debt relief?

Yes, provided that the interest you save during the promotional window outweighs the upfront transfer fee, and you remain disciplined enough to clear the balance before the regular APR takes effect.

2. Can I transfer a balance between two different Capital One cards?

No. Capital One explicitly prohibits transferring balances between accounts issued by Capital One or any of its corporate affiliates.

3. Will initiating a balance transfer damage my credit score?

The initial application requires a hard credit inquiry, which can cause a small, temporary dip in your score. However, systematically lowering your overall credit utilization through steady repayments generally benefits your score over the long run.

4. What happens when the promotional 0% APR period expires?

The card’s standard regular variable APR will automatically apply to any remaining unpaid balance. It is critical to structure your repayment strategy so that the balance hits zero before this window closes.

“For more information and official guidelines regarding balance transfers, you can visit the Consumer Financial Protection Bureau – Guide to Credit Cards.”

Disclaimer: Credit card terms, interest rates, and promotional offers change frequently. This content is intended for educational purposes and does not guarantee card approval or specific financial savings. Always verify live pricing and terms directly on the official Capital One website before submitting an application.

“Hi, I am Devel Gupta, an entrepreneur and the founder of FinanceWithDevel. With 10 years of experience in teaching and simplifying personal finance, my mission is to help beginners build long-term wealth without the confusing jargon. Whether it’s budgeting, investing, or retirement planning, I believe financial freedom starts with simple, consistent habits. Let’s make money make sense. Connect with me on [ LinkedIn/Twitter ] for more daily tips!”