Key takeaways

- For most people, the safest answer is not either-or. Start with a small cash cushion, then attack costly debt.

- If you have no savings, build a starter fund before sending every extra dollar to lenders.

- If you already have basic savings, high-interest credit card debt should usually come next.

- The best choice depends on your income, interest rates, bills, and how likely you are to face surprise expenses.

- Treat emergency fund or pay off debt in 2026 as a planning question, not a guilt trip.

Emergency Fund or Pay Off Debt in 2026

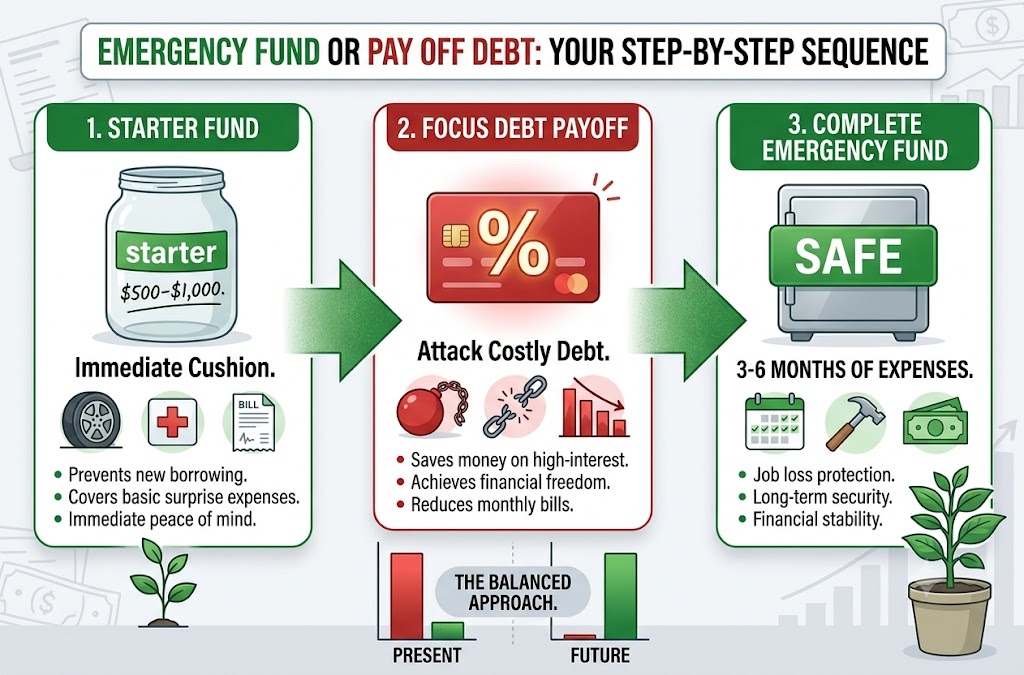

When people ask whether they should build an emergency fund or pay off debt in 2026, my answer is simple: do both, but in the right order. First, save a small starter fund of $500 to $1,000. That money can stop a flat tyre, urgent prescription, or surprise utility bill from landing back on a credit card.

After that, focus hard on expensive debt. If your credit card charges around 20% interest, carrying a balance each month is costly. A savings account may help you feel safe, but it usually cannot beat the cost of high-interest debt. The smart move is balance, not panic.

Why this question matters more in 2026

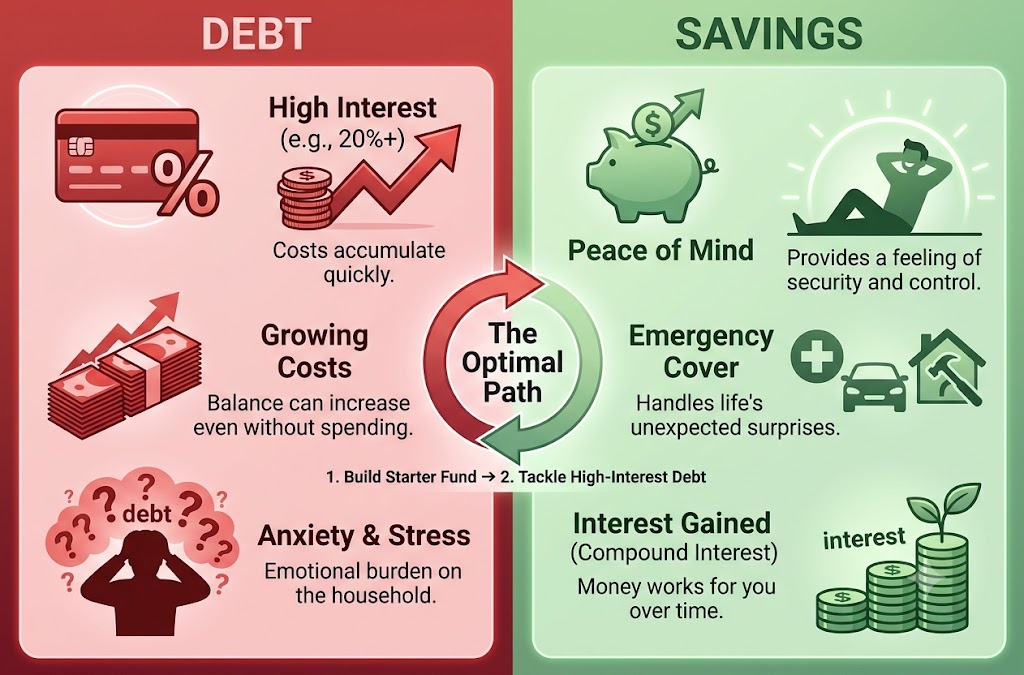

The debate over emergency fund or pay off debt in 2026 matters because household budgets still feel tight. Rent, insurance, groceries, utilities, and car costs have made “normal” monthly spending harder to predict. At the same time, credit cards remain expensive for many borrowers, so balances can quietly eat into a paycheck.

There is also a behaviour side to this. If you throw every spare dollar at debt but have no cash, the next emergency may push you right back into borrowing. That feels like running on a treadmill: lots of effort, no progress. A small emergency fund gives you breathing room, while debt payoff gives you long-term freedom.

What is an emergency fund?

An emergency fund is money set aside only for real surprises. Think job loss, medical bills, car repairs, home repairs, or a sudden family trip you cannot avoid. It is not vacation money, shopping money, or “I found a great sale” money.

For most U.S. households, the first target is a starter fund. That may be $500, $1,000, or one month of basic expenses. Once expensive debt is under control, the stronger goal is three to six months of essential expenses. Keep this money somewhere safe and easy to access, such as a savings account, not in stocks.

What counts as debt?

Debt is any money you owe, but not all debt deserves the same urgency. Credit cards, payday loans, and some personal loans are often the most dangerous because the interest can be high. Medical debt, student loans, auto loans, and mortgages may need a different plan depending on rates and repayment terms.

When deciding on emergency fund or pay off debt in 2026, look at the interest rate first. A 24% credit card balance is not the same as a 5% car loan. Minimum payments also matter. If you are close to missing payments, protecting your credit and avoiding late fees should become a priority.

Emergency fund vs debt payoff: Quick comparison table

| Choice | Best for | Main benefit | Main risk |

| Build emergency savings first | No savings, unstable income, frequent surprise bills | Prevents new debt | Debt interest keeps growing |

| Pay debt first | High-interest credit cards or payday loans | Saves money on interest | No cash backup |

| Do both together | Most households | Builds safety while reducing debt | Progress may feel slower |

Who should build an emergency fund first?

Choose savings first if you have almost no cash cushion. If one small emergency would force you to borrow, you need a starter fund before aggressive debt payoff. This is especially true if your income changes month to month, you are self-employed, or your job feels uncertain.

The emergency fund or pay off debt in 2026 decision also leans toward savings if you have kids, an older car, medical costs, or a home that needs repairs. These situations create surprise expenses often. Start with a small goal, automate a weekly transfer, and keep it boring. Boring money is often the money that saves you.

Who should pay off debt first?

Paying off debt first makes sense when you already have a small emergency fund, and your debt is expensive. Credit card debt is the obvious example. If you owe $5,000 at a high APR, waiting too long can cost hundreds or even thousands in interest.

This is where emergency fund or pay off debt in 2026 becomes a math problem. Pay minimums on everything, then send extra money to the highest-interest balance. If motivation matters more than math, you can use the debt snowball method and pay the smallest balance first. To understand which strategy fits you best, check out our guide on Debt Snowball vs Avalanche: Best Way to Pay Off Credit Card Debt in 2026. The key is having a clear payoff date…”

Why high-interest debt should not be ignored

High-interest debt is like a leak under the sink. You may not see damage every day, but it gets worse while you ignore it. A credit card balance can grow even when you stop spending because interest keeps adding to the bill.

That is why emergency fund or pay off debt in 2026 is not only an emotional question. It is a numbers question too. If your savings earns a small return but your card charges a much higher rate, the debt is winning. Keep enough cash to avoid new borrowing, then attack the expensive balance.

How much emergency fund should you have in 2026?

Start with a number you can actually reach. For many people, $500 is a solid first step. Then aim for $1,000. After that, try one month of rent, utilities, groceries, insurance, gas, and minimum debt payments.

Once high-interest debt is lower, build toward three to six months of essential expenses. If you have one income, irregular work, health concerns, or dependents, lean closer to six months. If your job is stable and your debt is expensive, one month may be enough while you focus on payoff. That is the practical middle ground in the emergency fund or pay off debt in 2026 decision.

When to do both at the same time

Many readers do not need a perfect either-or answer. The best plan for emergency fund or pay off debt in 2026 may be splitting extra money. For example, if you have $300 left after bills, put $100 into savings and $200 toward your highest-interest debt.

This works well when you need emotional safety and financial progress. You see savings grow, but you also see debt fall. That small win on both sides can help you stay consistent, and consistency beats a perfect plan you quit after three weeks.

A practical strategy: Save a small emergency fund, then attack debt

Here is a simple plan I would give a friend:

- Pay all minimum payments on time.

- Save a starter emergency fund of $500 to $1,000.

- List debts by interest rate.

- Put extra money toward the highest-interest debt.

- Keep using a small monthly transfer to savings.

- After high-interest debt is gone, build three to six months of expenses.

This approach keeps the emergency fund or pay off debt in 2026 decision grounded. You are not choosing fear over math or math over real life. You are using both.

Example: Credit card debt vs emergency savings

Say Maria lives in Ohio, earns $4,200 a month after taxes, has $300 in savings, and owes $6,000 on a credit card. Her rent, groceries, insurance, gas, utilities, and minimum payments total about $3,600. She has around $600 left in a normal month.

Maria should not put the full $600 toward debt right away. First, she could save $400 a month for two months and reach about $1,100 in emergency savings. Then she could shift to $100 into savings and $500 toward the card. For Maria, emergency fund or pay off debt in 2026 is not a debate; it is a sequence.

Mistakes to avoid

- Waiting to save until all debt is gone.

- Saving too much while paying 20%+ credit card interest.

- Making only minimum payments with no payoff date.

- Using emergency savings for non-emergencies.

- Ignoring late fees, overdraft fees, and missed-payment damage.

- Forgetting to check whether a balance transfer or lower-rate loan could help.

Disclaimer

This article is educational and does not give personal financial advice. Your best choice depends on your income, debt terms, credit score, family needs, taxes, and risk level. Consider speaking with a qualified financial planner or nonprofit credit counsellor before making major financial decisions.

Final verdict: emergency fund or pay off debt in 2026?

The clearest answer is this: build a small emergency fund first, then focus hard on high-interest debt, while still saving a little each month. If you have zero savings, debt payoff alone can backfire. If you have a solid cash cushion but expensive credit card debt, saving more while interest piles up can slow you down.

So, when choosing emergency fund or pay off debt in 2026, do not look for a one-size-fits-all rule. Start with safety, then chase interest savings. A small cushion protects your present. Debt payoff protects your future. Together, they give your budget room to breathe.

FAQs

Should I save money if I have credit card debt?

Yes, but start small. Build a starter fund first, then focus most extra money on the credit card balance.

Is $1,000 enough for an emergency fund in 2026?

It is a good starter fund, not a full emergency fund. The bigger goal is one month of expenses, then three to six months.

Should I use my emergency fund to pay off debt?

Usually, do not drain it completely. Keeping some cash can prevent new debt when the next surprise bill arrives.

What debt should I pay first?

Start with the highest-interest debt, especially credit cards or payday loans. This usually saves the most money.

Can I invest while paying off debt?

Yes, especially if you get a 401(k) match. But high-interest debt should usually be paid off before additional investing.

“Hi, I am Devel Gupta, an entrepreneur and the founder of FinanceWithDevel. With 10 years of experience in teaching and simplifying personal finance, my mission is to help beginners build long-term wealth without the confusing jargon. Whether it’s budgeting, investing, or retirement planning, I believe financial freedom starts with simple, consistent habits. Let’s make money make sense. Connect with me on [ LinkedIn/Twitter ] for more daily tips!”