Introduction

If you want to master how to calculate FIRE number in 2026, you are taking the first real step toward total control of your time. Think of this number as the exact price tag on your financial freedom. Once you lock in this target, every dollar you save, invest, and budget gets a clear, actionable purpose. Here is exactly how to find your baseline benchmark

The Goal: It’s not just about quitting work forever; it means having enough invested to change careers, start a business, or travel without worrying about a paycheck.

The Reality: A vague dream like “I want to retire early” becomes an actionable plan once you turn it into a measurable dollar amount.

The Timeline: Knowing this baseline benchmark helps you accurately test your savings plan against your risk tolerance and future spending goals.

What Is a FIRE Number?

A FIRE number is the exact amount of invested money you need to support your annual lifestyle expenses without depending on active employment income. It typically includes stocks, bonds, index funds, and retirement accounts, but excludes emergency cash or money needed for near-term goals. Understanding how to calculate FIRE number in 2026 is crucial because it turns a vague dream like “I want to retire early” into a clear, measurable financial target.

For example, if your annual lifestyle costs $60,000, applying the standard 25x rule sets your basic baseline at $1.5 million. Hitting this number doesn’t mean you are forced to stop working immediately; rather, it gives you a powerful, concrete benchmark to test against your personal timeline, risk tolerance, and future spending plans.

Step-by-Step: How to Calculate FIRE Number in 2026

Finding your retirement target comes down to four simple steps:

Track your annual expenses: Start with your current spending, then add potential future costs like independent health insurance or travel.

Subtract passive income: Deduct reliable income sources (like rental income or pensions) from your total expenses.

Choose your withdrawal rate: A standard 4% rate is common, but a safer 3.5% rate offers a bigger cushion for early retirement.

Run the math: Multiply your adjusted annual expenses by 25 (for the 4% rule) to get your baseline number.

The Formula: How to Calculate FIRE Number in 2026

The classic formula for How to Calculate FIRE Number in 2026 is simple: Annual expenses × 25 = FIRE number. This is based on a 4% withdrawal rate because dividing by 4% is the same as multiplying by 25. For example, if you expect to spend $50,000 per year, the 25x rule gives you a FIRE number of $1,250,000. The more flexible formula is Annual expenses ÷ safe withdrawal rate = FIRE number. If you prefer a 3.5% withdrawal rate, the same $50,000 lifestyle would need about $1,428,571. That gap matters because early retirees may need their portfolio to last 40 or 50 years, not just 30.

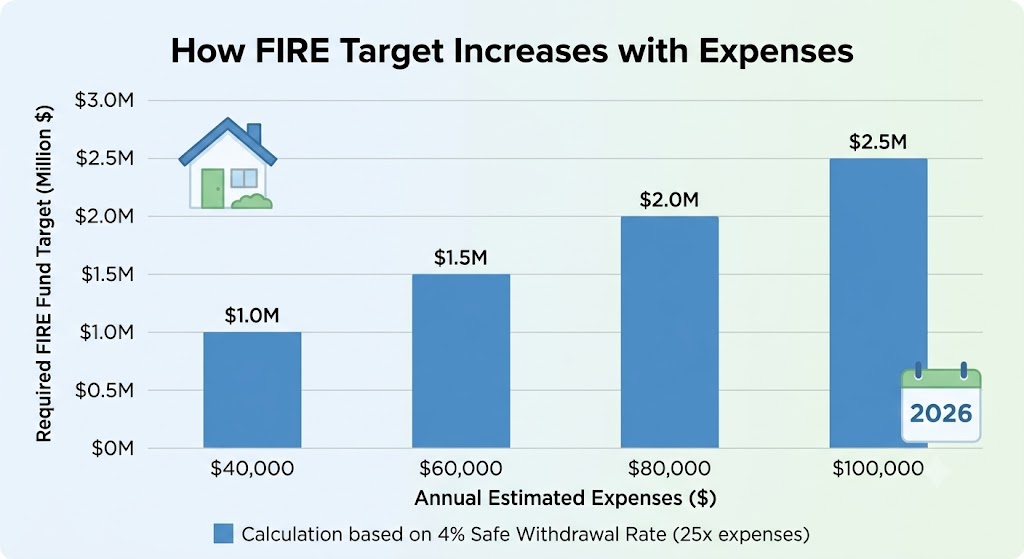

FIRE Number Example Table

Use this table as a beginner-friendly snapshot for How to Calculate FIRE Number in 2026. The 4% column is the simple 25x rule. The 3.5% column is more conservative and may fit someone who wants a bigger safety margin.

| Expected Annual Expenses | 4% Rule / 25x Target | 3.5% Withdrawal Target |

| $ 40,000 | $ 10,00,000 | $ 11,42,857 |

| $ 60,000 | $ 15,00,000 | $ 17,14,286 |

| $ 80,000 | $ 20,00,000 | $ 22,85,714 |

| $ 1,00,000 | $ 25,00,000 | $ 28,57,143 |

💡 Nerd Tip: If you plan to retire before age 50, your portfolio needs to last 40 to 50 years instead of the traditional 30. Consider using a conservative 3.5% withdrawal rate (multiplying your expenses by ~28.5) to protect against long-term inflation and market drops.

Real-Life Example

Here is a practical example of How to Calculate FIRE Number in 2026. Imagine Maya, age 35, spends $5,500 per month in Texas, including rent, groceries, insurance, transportation, travel, and fun money. Her annual spending is $66,000. Using the 25x rule, Maya’s FIRE number is $1,650,000. But she wants to retire before 50, so she uses a 3.5% withdrawal rate for extra caution. Her target becomes $66,000 ÷ 0.035, or about $1,885,714. Maya rounds that to $1.9 million, then builds a plan around maxing retirement accounts, investing in low-cost index funds, keeping a taxable brokerage account for early-retirement access, and reviewing her number every year.

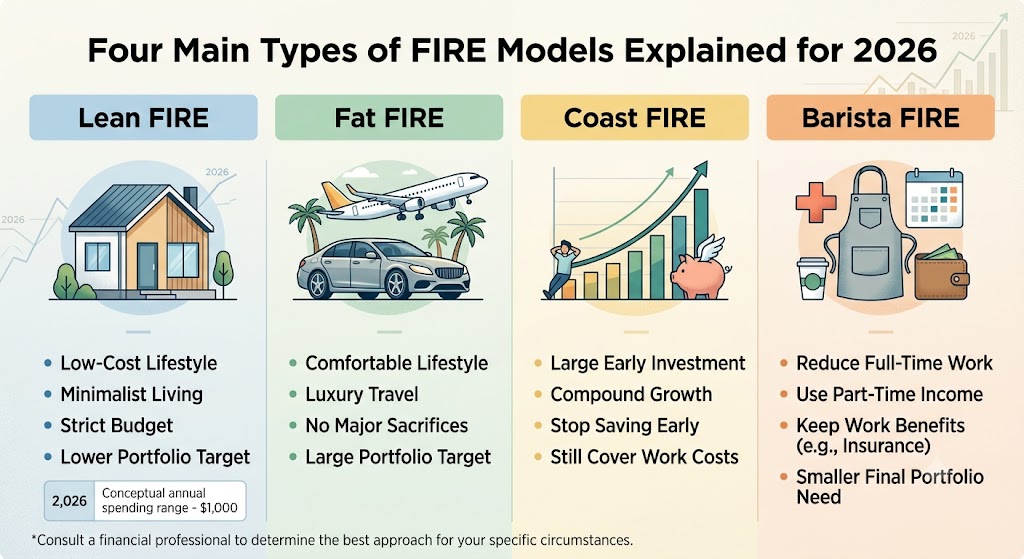

Types of FIRE: Lean FIRE, Fat FIRE, Coast FIRE, and Barista FIRE

How to Calculate FIRE Number in 2026 also depends on which version of FIRE fits your lifestyle and future goals:

Lean FIRE: Retiring with a lower-cost, minimalist lifestyle by heavily cutting housing, transportation, or discretionary spending.

Fat FIRE: Building a much larger portfolio to support a comfortable lifestyle with luxury travel, fine dining, healthcare flexibility, and fewer sacrifices.

Coast FIRE: Investing heavily early on so that your portfolio can “coast” and grow to your target via compound interest, allowing you to stop aggressive saving and just cover daily costs.

Barista FIRE: Saving enough to quit your corporate 9-to-5, but working a part-time or low-stress job to cover baseline health insurance or daily expenses.

None of these is “best” for everyone; the right version is simply the one you can realistically live with.

Common Mistakes to Avoid

One big mistake in How to Calculate FIRE Number in 2026 is using today’s spending without thinking about tomorrow’s reality. Your rent may rise, health insurance may cost more, children may change your budget, and taxes can reduce what you actually keep. Another mistake is counting home equity as if it automatically pays grocery bills. A paid-off house can lower expenses, but unless you sell it, rent part of it, or borrow against it, it does not act like an investment portfolio. People also forget about sequence-of-returns risk, which is the danger of retiring right before a bad market stretch. A smart FIRE plan leaves room for cash reserves, flexible spending, and a backup income plan.

How to Adjust Your FIRE Number for 2026

The smartest way to approach How to Calculate FIRE Number in 2026 is to update your number once or twice a year. Inflation can quietly move the goalpost, especially when essentials like energy, food, rent, and insurance rise faster than your budget expected. Retirement contribution limits also matter because higher limits may help U.S. savers shelter more money in tax-advantaged accounts. If you use a 401(k), IRA, HSA, or taxable brokerage account, your FIRE plan should show which accounts you will use before age 59½ and which ones you will leave for later. A good 2026 adjustment is to run three targets: basic FIRE, comfortable FIRE, and conservative FIRE.

What to Do After Finding Your FIRE Number

Once you understand How to Calculate FIRE Number in 2026, turn the number into a monthly action plan. First, build or protect an emergency fund so one surprise bill does not force you to sell investments at the wrong time. Next, pay down high-interest debt because credit card interest can destroy progress faster than investing can repair it. Then automate investing into retirement accounts and taxable brokerage accounts based on your timeline. Track your savings rate, not just your income, because FIRE is powered by the gap between what you earn and what you keep. Finally, review your plan every year and ask: Is my spending still accurate? Is my portfolio diversified? Is my withdrawal rate still reasonable?

Disclaimer

This article about How to Calculate FIRE Number in 2026 is for educational purposes only and is not financial, tax, legal, or investment advice. FIRE planning depends on your income, expenses, age, tax situation, health, family responsibilities, risk tolerance, and investment choices. Before making major retirement or investment decisions, consider speaking with a qualified financial planner or tax professional.

Conclusion

Finding your FIRE number isn’t about hitting a rigid, perfect milestone—it’s about locking in a flexible freedom target that grows with your life. While the baseline math is as simple as multiplying your expenses by 25, the real magic happens when you adjust that number for real-world realities like inflation, taxes, and healthcare.

If your final target looks intimidating at first glance, don’t panic. Let how to calculate FIRE number in 2026 serve as an inspiring blueprint rather than a roadblock. Financial independence is built one intentional decision at a time: automate your investments, curb lifestyle creep, keep tracking your savings rate, and watch your freedom look closer every single year.

FAQs

1. What is the easiest way to start?

The easiest way is to track your monthly spending for three to six months, multiply it by 12, then multiply annual expenses by 25. How to Calculate FIRE Number in 2026 can start as a rough estimate before you refine taxes, inflation, and health care. That gives you a quick starting estimate.

2. Is the 4% rule still useful?

Yes, but use it as a guide, not a promise. A lower withdrawal rate may be safer for early retirees with longer timelines.

3. Does my FIRE number include my home?

Usually, no. Your home can reduce expenses if it is paid off, but it does not pay bills unless it creates cash flow or you sell it.

4. How often should I update my FIRE number?

Review it at least once a year, and update it after major life changes such as marriage, children, a move, a new job, or a big market shift.

5. Why is How to Calculate FIRE Number in 2026 different from older FIRE planning?

It requires more attention to inflation, health care, taxes, withdrawal-rate flexibility, and account access because early retirement can last much longer than traditional retirement.

“To learn more about managing your money before retiring, check out our guide on

(https://financewithdevel.com/blog/).

“Hi, I am Devel Gupta, an entrepreneur and the founder of FinanceWithDevel. With 10 years of experience in teaching and simplifying personal finance, my mission is to help beginners build long-term wealth without the confusing jargon. Whether it’s budgeting, investing, or retirement planning, I believe financial freedom starts with simple, consistent habits. Let’s make money make sense. Connect with me on [ LinkedIn/Twitter ] for more daily tips!”